👨🏫 Outline

📖 Berk, DeMarzo and Harford Chap. 13

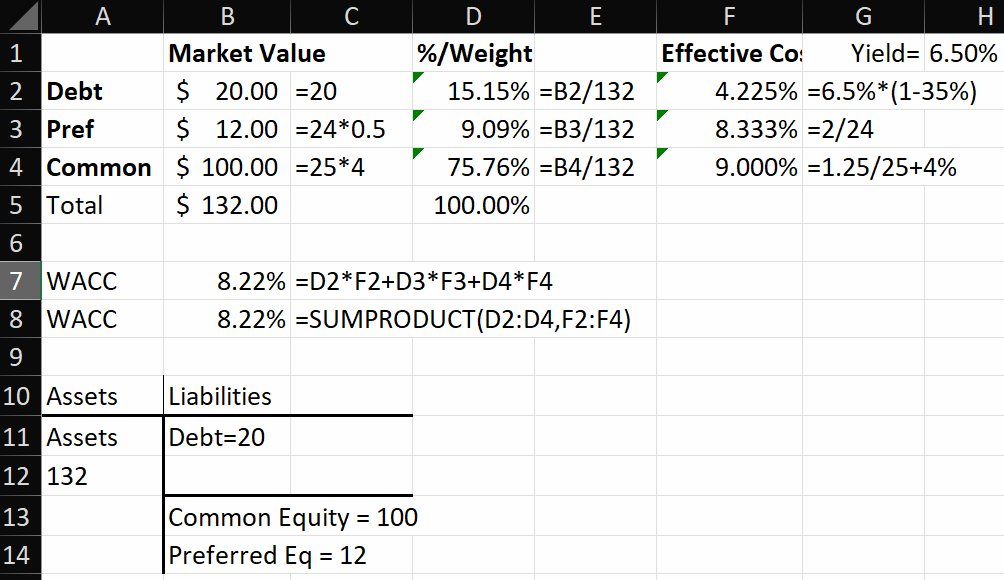

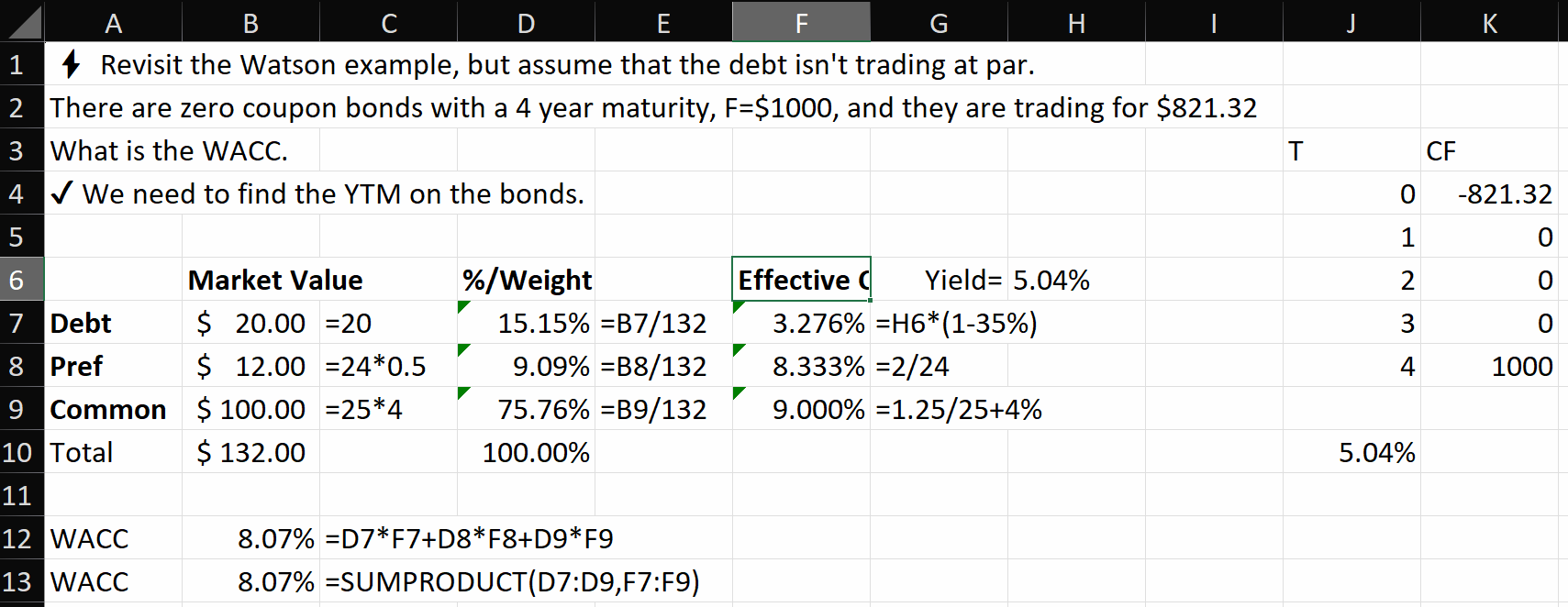

A great thing about this lecture is that almost all of it is devoted to teaching different skills used in calculating the WACC. Students asked for a single example that integrates all of these skills into one problem. This example problem can be found on the Watson Company WACC page

The main notes for this material are at: 🔎 Understanding WACC

2. Weights = Percent of Mkt Val

3. Multiply Weights × Effective Rates

4. Add together for weighted average

- A = 1.8B + 1B*13.2 = 15

- D% = 1.8/15 = 12%,

E% = 13.2/15 = 88% - WACC=12%*7% + 88%*9% = 8.76%

1) Capital Asset Pricing Model (CAPM)

2) Constant Div. Growth Model (CDGM)

= rf + β(Risk Prem on Mkt)

= (div (1yr)/ stock price) + est. growth rate

= 2.81/92+4% = .0705 or 7.05%

= 3.5B

= 3.4B

Risk Premium = Expected Rate - Risk Free Rate

B = Beta

E(rm) = Expected Return of the Market

E(r) = Expected Return of Stock

g = Growth Rate

PB = Bond price

F = Face Value

Outline of lecture 7: Cost of Capital

Section titled “Outline of lecture 7: Cost of Capital”- The Firm’s Cost of Debt Capital

- The effective cost of debt

- The Firms Cost of Equity Capital

- The cost of common stock capital

- The cost of preferred stock capital

- The Weighted Average Cost of Capital (WACC)

Learning Objectives

Section titled “Learning Objectives”- Understand the drivers of the firm’s overall cost of capital

- Measure the costs of debt, preferred stock, and common stock

- Compute a firm’s overall, or weighted average, cost of capital

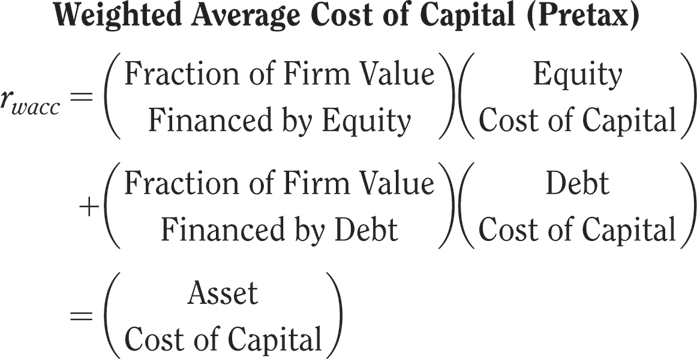

Overall Cost of Capital

Section titled “Overall Cost of Capital”Commonly referred to as the

- Weighted Average Cost of Capital (WACC)

As the name suggests, the WACC is a weighted average of the costs of capital from each of the firm’s sources of financing.

- Debt

- Equity

- Common stock

- Preferred stock

The WACC may be appropriate to use as the discount rate when calculating the NPV of a project.

However, for some projects, the WACC may need to be adjusted in order to serve as the discount rate.

A First Look at the Weighted Average Cost of Capital

Section titled “A First Look at the Weighted Average Cost of Capital”- Weighted Average Cost of Capital Calculations

- The Weighted Average Cost of Capital: Unlevered Firm

- rWACC = Equity Cost of Capital

- The Weighted Average Cost of Capital: Levered Firm

- The Weighted Average Cost of Capital: Unlevered Firm

Example: Calculating the Weights in the WACC

Section titled “Example: Calculating the Weights in the WACC”Problem:

- Suppose McDonalds Inc. has debt with a market value of $18 billion outstanding, and common stock with a market value of $52 billion and a book value of $36 billion. Which weights should McDonalds use in calculation of its WACC?

Solution:

Plan:

- The WACC equation tells us that the weights are the fractions of McDonalds assets financed with debt and financed with equity. We know these weights should be based on market values because the cost of capital is based on investors’ current assessment of the value of the firm, not their assessment of accounting-based book values. As a consequence, we can ignore the book value of equity.

Execute:

- Given its $18 billion in debt and $52 billion in equity, the total value of the firm is $70 billion.

Evaluate:

- When calculating its overall cost of capital, McDonalds will use a weighted average of the cost of its debt capital and the cost of its equity capital, giving a weight of 25.7% to its cost of debt and a weight of 74.3% to its cost of equity.

Problem:

- Suppose Kenai Corp. has debt with a book (face) value of $10 million, trading at 95% of face value. It also has book equity of $10 million, and 1 million shares of common stock trading at $30 per share. What weights should Kenai use in calculating its WACC?

Solution: Plan:

- The WACC equation tells us that the weights are the fractions of Kenai financed with debt and financed with equity. Furthermore, these weights should be based on market values because the cost of capital is based on investors’ current assessment of the value of the firm, not their assessment of accounting-based book values. As a consequence, we can ignore the book values of debt and equity.

Execute:

- Ten million dollars in debt trading at 95% of face value is $9.5 million in market value. One million shares of stock at $30 per share is $30 million in market value. So, the total value of the firm is $39.5 million. The weights are:

Evaluate:

- When calculating its overall cost of capital, Kenai will use a weighted average of the cost of its debt capital and the cost of its equity capital, giving a weight of 24.1% to its cost of debt and a weight of 75.9% to its cost of equity.

Problem:

- Suppose 3M Corp. has debt with a book (face) value of $25 million, trading at 110% of face value. It also has book equity of $35 million, and 3 million shares of common stock trading at $25 per share. What weights should 3M use in calculating its WACC?

Solution:

Plan:

- The equation above tells us that the weights are the fractions of 3M financed with debt and financed with equity. Furthermore, these weights should be based on market values because the cost of capital is based on investors’ current assessment of the value of the firm, not their assessment of accounting-based book values. As a consequence, we can ignore the book values of debt and equity.

Execute:

- $25 million in debt trading at 110% of face value is $27.5 million in market value. Three million shares of stock at $25 per share is $75 million in market value. So, the total value of the firm is $102.5 million. The weights are:

Evaluate:

- When calculating its overall cost of capital, 3M will use a weighted average of the cost of its debt capital and the cost of its equity capital, giving a weight of 26.8% to its cost of debt and a weight of 73.2% to its cost of equity.

Problem:

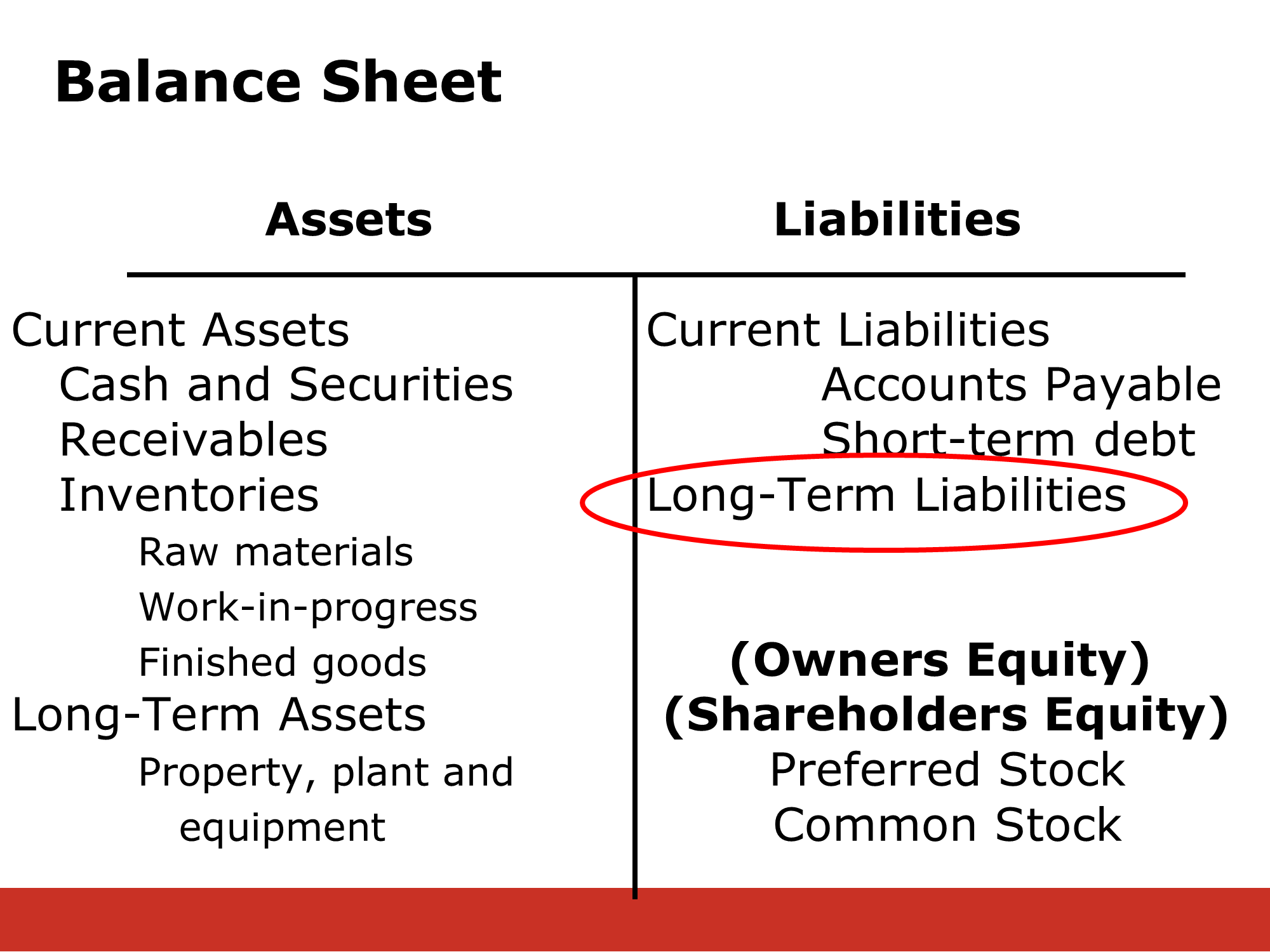

Suppose DigitalToiletPaper.com has the following balance sheet:

| Assets | Liabilities |

|---|---|

$14.3B | $6.8B |

Equity |

- Assuming the equity market-to-book ratio is 1.4, and that the firm’s debt is selling at 90% of its book value, what weights should Digital use in calculating its WACC?

Given that the firm’s debt is selling at a discount, it’s market value = .9 × $6.8B = $6.12B

We know that the equity value on the balance sheet is the equity book value. Given the market-to-book ratio of 1.4, the market value of equity = 1.4 × $7.5B = $10.5B

So the market value of the firm = $6.12B + $10.5B = $16.62B

Hence, the weight on debt = $6.12/$16.62 = .368 = 36.8%, and the weight on equity = $10.5/$16.62 = .632 = 63.2%

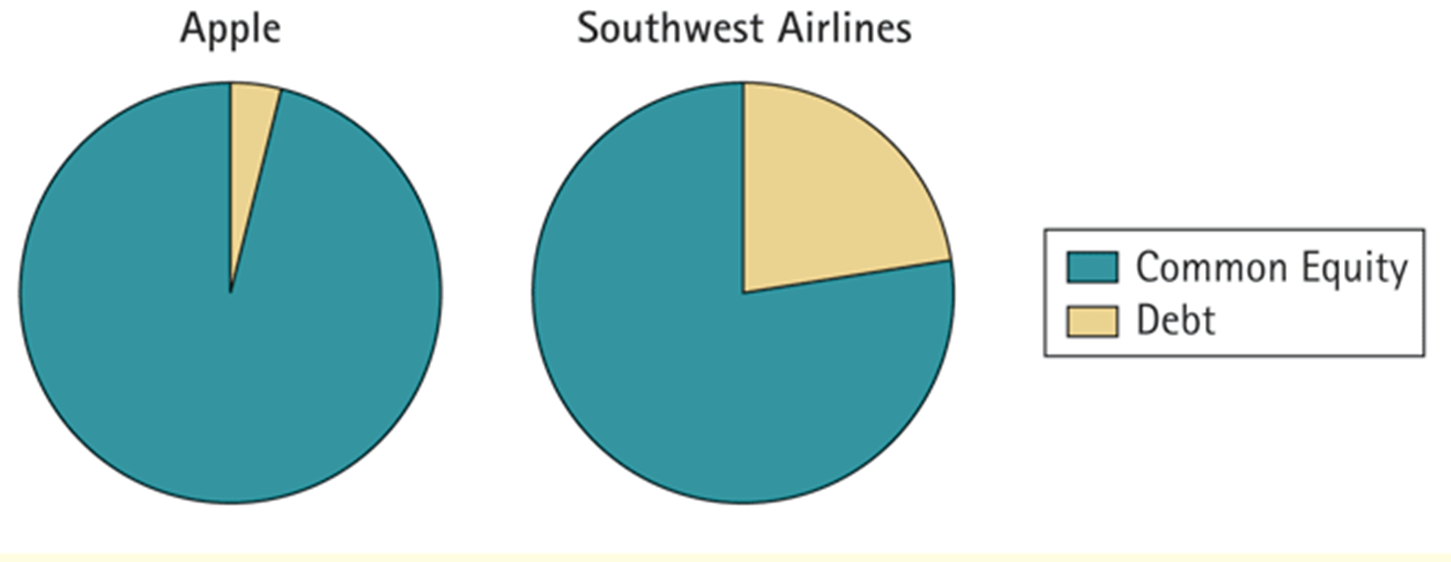

Extra Example: Two Capital Structures

Why do Apple and Southwest Airlines choose to have such different capital structures? In other words, why does Southwest choose to have so much more debt than Apple. As a preview, we will later discuss how technology companies tend to be riskier than older companies and therefore tend to carry less debt. Let’s do the foundations first!

The Firm’s Costs of Debt Capital

Section titled “The Firm’s Costs of Debt Capital”- Yield to Maturity and the Cost of Debt

- The Yield to Maturity is the yield that bond purchasers would earn if they held the debt to maturity and received all the payments as promised

- The Yield to Maturity is the yield that investors demand to hold the firm’s debt (new or existing)

- Taxes and the Cost of Debt

- Effective Cost of Debt

where TC is the corporate tax rate.

Example: Effective Cost of Debt

Section titled “Example: Effective Cost of Debt”Problem:

- By using the yield to maturity on DuPont’s debt, we found that its pre-tax cost of debt is 2.81%. If DuPont’s tax rate is 35%, what is its effective cost of debt?

Solution:

Plan:

- We can calculate DuPont’s effective cost of debt:

Execute:

- DuPont’s effective cost of debt is

Evaluate:

- For every $1000 it borrows, DuPont pays its bondholders 0.0281($1000) = $28.10 in interest every year. Because it can deduct that $28.10 in interest from its income, every dollar in interest saves DuPont 35 cents in taxes, so the interest tax deduction reduces the firm’s tax payment to the government by 0.35($28.10) = $9.83. Thus DuPont’s net cost of debt is the $28.10 it pays minus the $9.83 in reduced tax payments, which is $18.27 per $1000 or 1.827%.

Cost of Preferred Stock Capital

Section titled “Cost of Preferred Stock Capital”- Assume DuPont’s class A preferred stock has a price of $66.67 and an annual dividend of $3.50. Its cost of preferred stock, therefore, is $3.50 ÷ $66.67 = 5.25%

Cost of Common Stock Capital

Section titled “Cost of Common Stock Capital ”Capital Asset Pricing Model

Section titled “Capital Asset Pricing Model”- Estimate the firm’s beta of equity, typically by regressing 60 months of the company’s returns against 60 months of returns for a market proxy such as the S&P 500

- Determine the risk-free rate, typically by using the yield on Treasury bills or bonds

Fundamental CAPM Equation

Section titled “Fundamental CAPM Equation”- Expected risk premium on stock = E(rS) - rF

- Expected risk premium on market = E(rM) - rF

Finance Jargon: Beta

Section titled “Finance Jargon: Beta”Beta (β) can be estimated with historical data

- Represents non-diversifiable risk, for which investors must be compensated

- For the market as a whole, β = 1

- β > 1 implies stock requires a return greater than the market return, because the stock is riskier (has a higher standard deviation) than the market

- β < 1 implies stock requires a return lower than the market return, because the stock is less risky (has a lower standard deviation) than the market

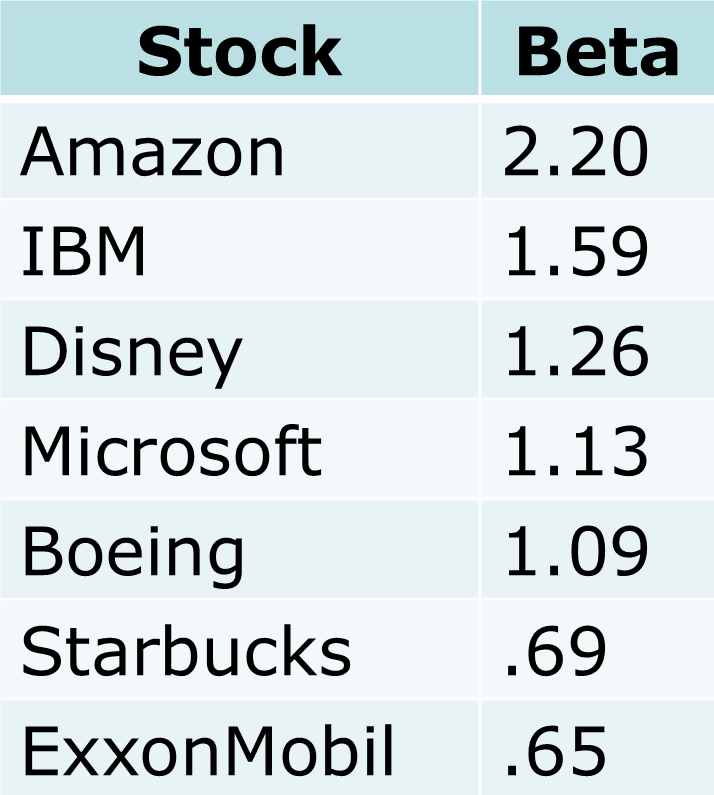

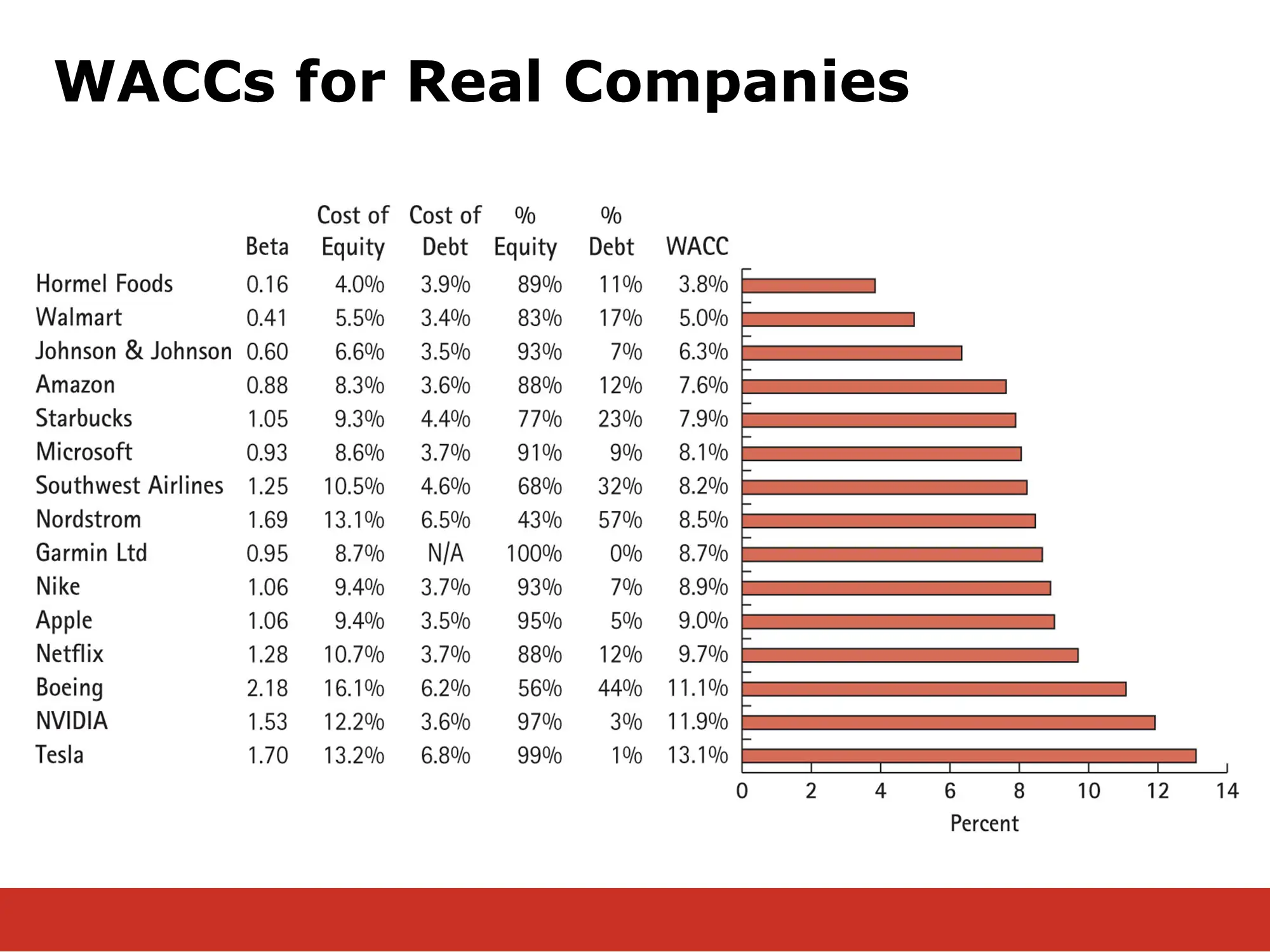

Betas for Some U.S. Stocks (Est. from data from 2001 - 2006)

Section titled “Betas for Some U.S. Stocks (Est. from data from 2001 - 2006)”

Assume:

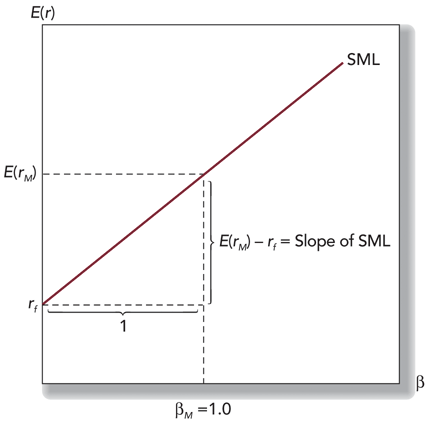

The Security Market Line

Section titled “The Security Market Line”

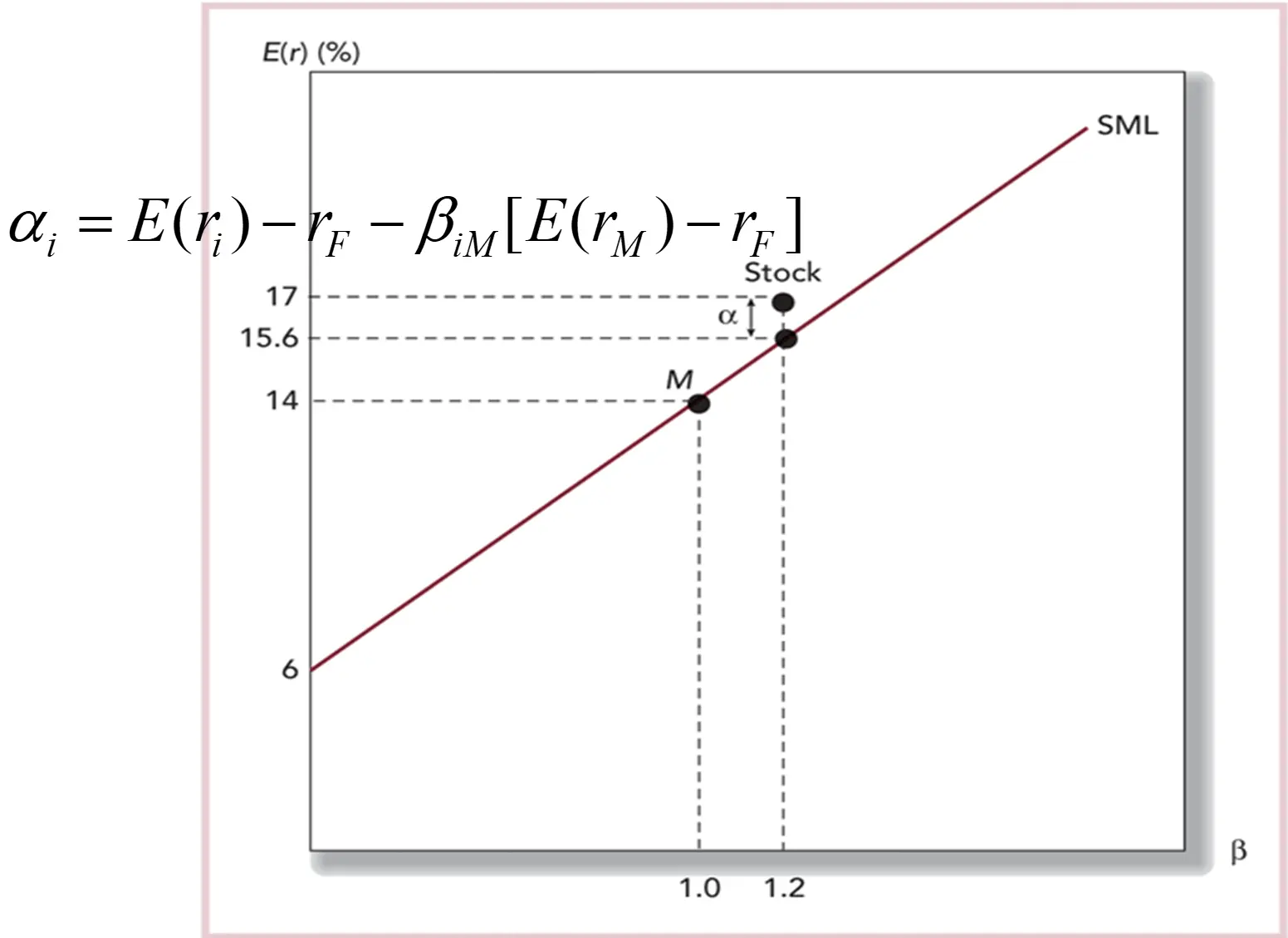

Alpha, Beta and the CAPM

Section titled “Alpha, Beta and the CAPM”In other words, if we do a regression of excess returns for asset i on the market excess return and estimate the coefficients:

where

αi (sometimes called “Jensen’s alpha”) should be zero for all assets iThe SML and a Positive-Alpha Stock

Section titled “The SML and a Positive-Alpha Stock”

Measuring the Cost of Equity

Section titled “Measuring the Cost of Equity”- Estimating Beta

- SML shows relationship between return and risk

- CAPM uses beta as proxy for risk

- Other methods can also determine slope of SML and beta

- Regression analysis can be used to find beta

Steps to use the CAPM

Section titled “Steps to use the CAPM”- Estimate the firm’s beta of equity, typically by regressing 60 months of the company’s returns against 60 months of returns for a market proxy such as the S&P 500

- Determine the risk-free rate, typically by using the yield on Treasury bills or bonds

- Estimate the market risk premium, typically by comparing historical returns on a market proxy to contemporaneous risk-free rates

- Apply the CAPM: Cost of Equity = Risk-Free Rate + Equity Beta × Market Risk Premium

- Assume the equity beta of DuPont is 1.37, the yield on ten-year Treasury notes is 3%, and you estimate the market risk premium to be 6%. DuPont’s cost of equity is 3% + 1.37 × 6% = 11.22%

Constant Dividend Growth Model (CDGM)

Section titled “Constant Dividend Growth Model (CDGM)”- Assume in mid-2013, the average forecast for DuPont’s long-run earnings growth rate was 7.9%. With an expected dividend in one year of $1.80 and a price of $57.66, the CDGM estimates DuPont’s cost of equity as follows (using Eq. 13.5):

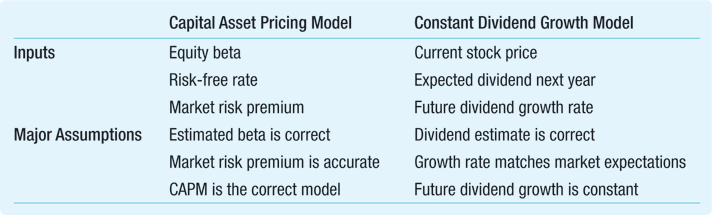

CAPM vs CDGM

Section titled “CAPM vs CDGM”

Example: Estimating the Cost of Equity

Section titled “Example: Estimating the Cost of Equity”Problem:

Assume the equity beta for Johnson & Johnson (ticker: JNJ) is 0.55. The yield on 10-year treasuries is 3%, and you estimate the market risk premium to be 6%. Furthermore, Johnson & Johnson issues dividends at an annual rate of $2.81. Its current stock price is $92.00, and you expect dividends to increase at a constant rate of 4% per year. Estimate J&J’s cost of equity in two ways

Solution:

Plan:

- The two ways to estimate J&J’s cost of equity are to use the CAPM and the CDGM.

- The CAPM requires the risk-free rate, an estimate of the equity’s beta, and an estimate of the market risk premium. We can use the yield on ten-year Treasury bills as the risk-free rate.

- The CDGM requires the current stock price, the expected dividend next year, and an estimate of the constant future growth rate for the dividend:

| Risk-free rate: 3% | Current price $92.00 |

| Equity beta: 0.55 | Expected dividend $2.81 |

| Market risk premium: 6% | Estimated future dividend growth rate: 4% |

- We can use the CAPM from Chapter 11 to estimate the cost of equity using the CAPM approach and Eq. 13.5 to estimate it using the CDGM approach.

Execute:

- The CAPM says that

For J&J, this implies that its cost of equity is:

- The CDGM says

Evaluate:

- According to the CAPM, the cost of equity capital is 6.3%; the CDGM produces a result of 7.1%. Because of the different assumptions we make when using each method, the two methods do not have to produce the same answer—in fact, it would be highly unlikely that they would. When the two approaches produce different answers, we must examine the assumptions we made for each approach and decide which set of assumptions is more realistic. We can also see what assumption about future dividend growth would be necessary to make the answers converge. By rearranging the CDGM and using the cost of equity we estimated from the CAPM, we have:

- Thus, if we believe that J&J’s dividends will grow at a rate of 3.2% per year, the two approaches would produce the same cost of equity estimate.

Problem:

The equity beta for Harley-Davidson (HOG) is 2.3. The yield on 10-year treasuries is 2.0%, and you estimate the market risk premium to be 4.5%. Further, HOG issues an annual dividend of $0.40. Its current stock price is $23.76, and you expect dividends to increase at a constant rate of 6.0% per year. Estimate HOG’s cost of equity in two ways.

Solution:

Plan:

- The two ways to estimate HOG’s cost of equity are to use the CAPM and the CDGM.

- The CAPM requires the risk-free rate, an estimate of the equity’s beta, and an estimate of the market risk premium. We can use the yield on 10-year Treasury bills as the risk-free rate.

- The CDGM requires the current stock price, the expected dividend next year, and an estimate of the constant future growth rate for the dividend.

| Risk-free rate: 2.0% | Current price $23.76 |

| Equity beta: 2.3 | Expected dividend $0.40 |

| Market risk premium: 4.5% | Estimated future dividend growth rate: 6% |

- We can use the CAPM from Chapter 12 to estimate the cost of equity using the CAPM approach and Eq. 13.5 to estimate it using the CDGM approach.

Execute:

The CAPM says that

The CDGM says that

Evalute:

- According to the CAPM, the cost of equity capital is 12.35%; the CDGM produces a result of 7.68%. Because of the different assumptions we make when using each method, the two methods do not have to produce the same answer - in fact, it would be highly unlikely that they would. When the two approaches produce different answers, we must examine the assumptions we made for each approach and decide which set of assumptions is more realistic.

- We can also see what assumption about future dividend growth would be necessary to make the answers converge. By rearranging the CDGM and using the cost of equity we estimated from the CAPM, we have

- Thus, if we believe that Harley-Davidson’s dividends will grow at a rate of 10.67% per year, the two approaches would produce the same cost of equity estimate.

A Second Look at the Weighted Average Cost of Capital

Section titled “A Second Look at the Weighted Average Cost of Capital”WACC Equation

Section titled “WACC Equation”- For a company that does not have preferred stock, the WACC condenses to:

- In mid-2013, the market values of DuPont’s common stock, preferred stock, and debt were $53,240 million, $221 million, and $14,080 million, respectively. Its total value was, therefore, $53,240 million + $221 million + $14,080 million = $67,541. Given the costs of common stock, preferred stock, and debt we have already computed, DuPont’s WACC in late mid-2013 was:

Example: Computing the WACC

Section titled “Example: Computing the WACC”Problem:

- The expected return on Target’s equity is 11.5%, and the firm has a yield to maturity on its debt of 6%. Debt accounts for 18% and equity for 82% of Target’s total market value. If its tax rate is 35%, what is this firm’s WACC?

Solution:

Plan:

- We can compute the WACC using Eq. 13.7. To do so, we need to know the costs of equity and debt, their proportions in Target’s capital structure, and the firm’s tax rate. We have all that information, so we are ready to proceed.

Execute:

Evalute:

- Even though we cannot observe the expected return of Target’s investments directly, we can use the expected return on its equity and debt and the WACC formula to estimate it, adjusting for the tax advantage of debt. Target needs to earn at least a 10.1% return on its investment in current and new stores to satisfy both its debt and equity holders.

Problem:

- The expected return on Macy’s equity is 10.8%, and the firm has a yield to maturity on its debt of 8%. Debt accounts for 16% and equity for 84% of Macy’s total market value. If its tax rate is 40%, what is this firm’s WACC?

Solution:

Plan:

- We can compute the WACC using Eq. 13.7. To do so, we need to know the costs of equity and debt, their proportions in Macy’s capital structure, and the firm’s tax rate. We have all that information, so we are ready to proceed.

Execute:

Evalute:

- Even though we cannot observe the expected return of Macy’s investments directly, we can use the expected return on its equity and debt and the WACC formula to estimate it, adjusting for the tax advantage of debt. Macy’s needs to earn at least a 9.84% return on its investment in current and new stores to satisfy both its debt and equity holders.

Problem:

- The expected return on Honeywell International’s (HON) equity is 12.0%, and the firm has a yield to maturity on its debt of 5.1%. Debt accounts for 28% and equity for 72% of HON’s total market value. If its tax rate is 39%, what is this firm’s WACC?

Solution:

Plan:

- We can compute the WACC using Eq. 13.7. To do so, we need to know the costs of equity and debt, their proportions in HON’s capital structure, and the firm’s tax rate. We have all that information, so we are ready to proceed.

Execute:

Evaluate:

- Even though we cannot observe the expected return of Honeywell’s investments directly, we can use the expected return on its equity and debt and the WACC formula to estimate it, adjusting for the tax advantage of debt. Honeywell needs to earn at least a 9.51% return on its investment in current and new stores to satisfy both its debt and equity holders.

Feedback? Email robmgmte2700@gmail.com 📧. Be sure to mention the page you are responding to.