👨🏫 Notes

Income Statement

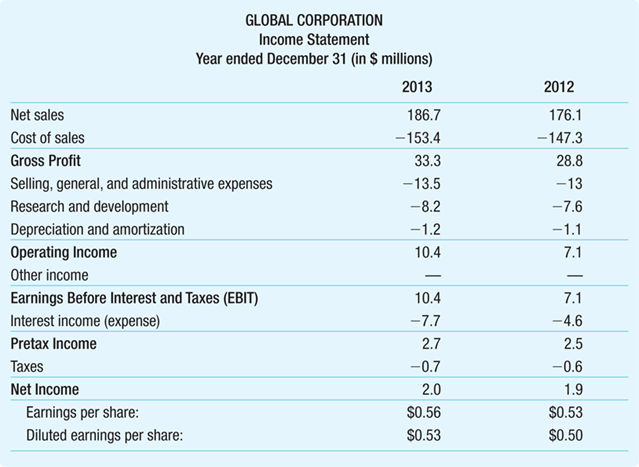

Section titled “Income Statement”The income statement lists the firm’s revenues and expenses over a period of time

- Sometimes called the profit and loss statement, or “P&L” The last or “bottom” line of the income statement shows net income

- A measure of its profitability during the period

- Also referred to as the firm’s earnings

Earnings Calculations

Section titled “Earnings Calculations”- Revenue (top line)

- Gross Profit

- Revenues (Net Sales) - Cost of Sales = Gross Profit

- Operating Expenses

- Gross Profit - Operating Expenses = Operating Income

- Earnings Before Interest and Taxes (EBIT)

- Operating Income +/- Other Income = Earnings Before Interest and Taxes

- Pretax and Net Income

- EBIT +/- Interest income (Expense) = Pretax Income

- Pretax Income - Taxes = Net Income

Earnings Per Share = Net income reported on a per-share basis

Fully diluted EPS increases number of shares by:

- Stock options issued to employees

- The right to buy a certain number of shares by a specific date at a specific price

- Shares issued due to conversion of convertible bonds

- Convertible bonds are corporate bonds with a provision that gives the bondholder an option to convert each bond into a fixed number of shares of common stock

EBITDA

Section titled “EBITDA”- Financial analysts often compute a firm’s earnings before interest, taxes, depreciation, and amortization, or EBITDA

- Because depreciation and amortization are not cash flows, this subtotal reflects the cash a firm has earned from operations

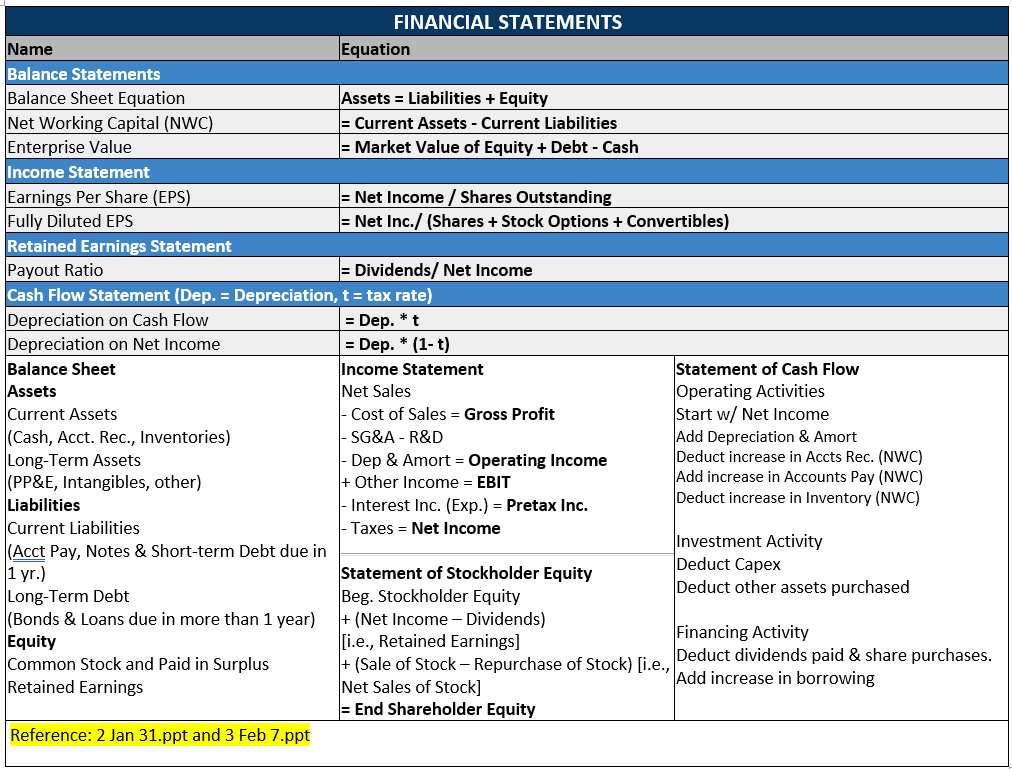

Statement of Cash Flows

Section titled “Statement of Cash Flows”The statement of cash flows is divided into three sections which roughly correspond to the three major jobs of the financial manager:

- Operating activities

- Investment activities

- Financing activities

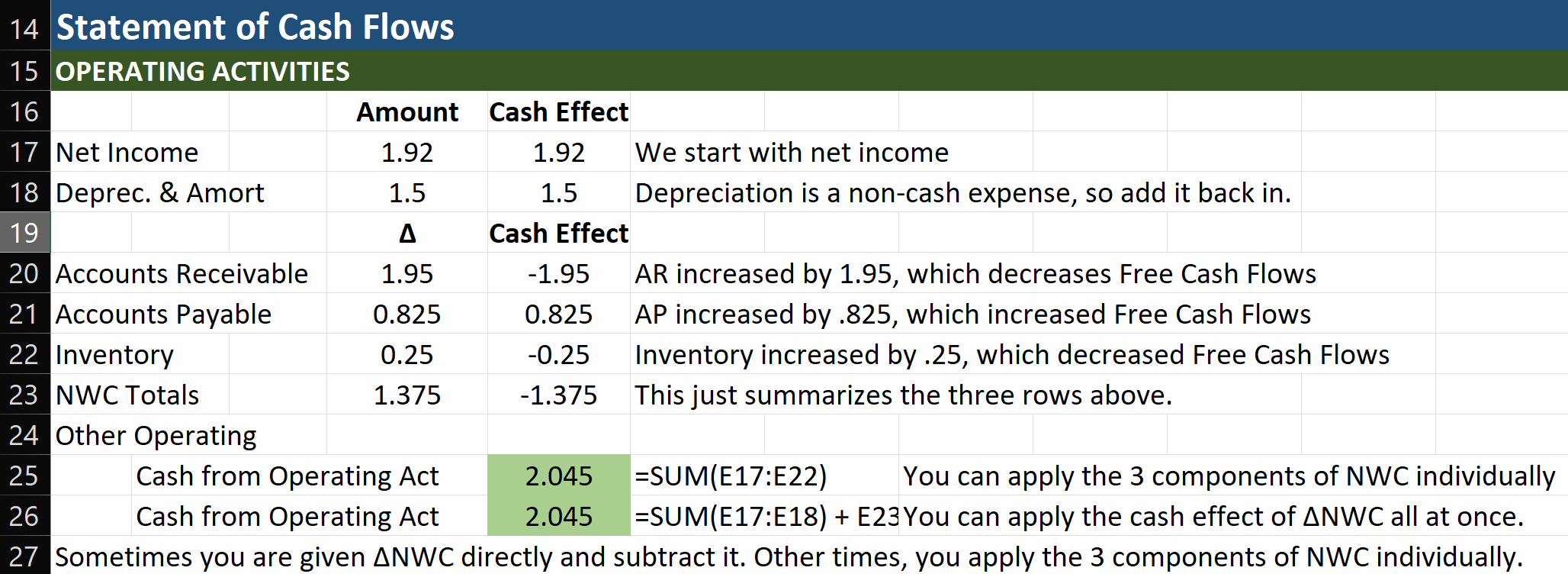

Statement of Cash Flows: Operating Activities

Section titled “Statement of Cash Flows: Operating Activities”

Depreciation:

Section titled “Depreciation:”- We also add depreciation to net income, since it is not a cash outflow

Accounts receivable:

Section titled “Accounts receivable:”- Adjust the cash flows by deducting the increases in accounts receivable

- This increase represents additional lending by the firm to its customers and it reduces the cash available to the firm

Accounts payable:

Section titled “Accounts payable:”- Similarly, we add increases in accounts payable

- Accounts payable represents borrowing by the firm from its suppliers

- This borrowing increases the cash available to the firm

Inventory:

Section titled “Inventory:”- Finally, we deduct increases to inventory

- Increases to inventory are not recorded as an expense and do not contribute to net income

- However, the cost of increasing inventory is a cash outflow for the firm and must be deducted on the statement of cash flows.

Statement of Cash Flows: Investment and Financing Activities

Section titled “Statement of Cash Flows: Investment and Financing Activities”Investment Activity

Section titled “Investment Activity”- Subtract the actual capital expenditure that the firm made

- Also deduct other assets purchased or investments made by the firm, such as acquisitions

Financing Activity

Section titled “Financing Activity”- The last section of the statement of cash flows shows the cash flows from financing activities

- Subtract Dividends paid

- Add cash received from sale of stock

- Subtract cash spent repurchasing your own stock

- Add changes to short-term and long-term borrowing

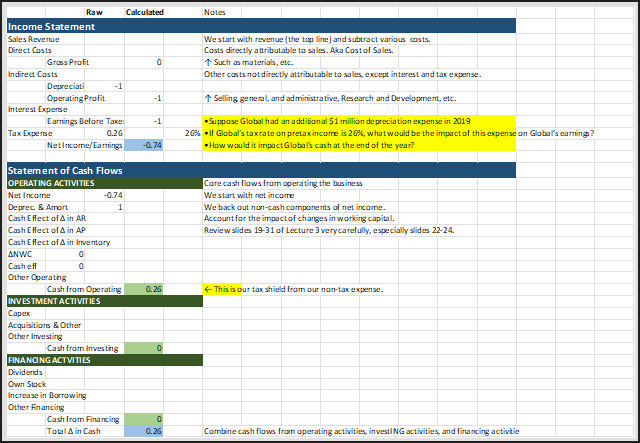

✏️ The Impact of Depreciation on Cash Flow

- Suppose Global had an additional $1 million depreciation expense in 2019

- If Global’s tax rate on pretax income is 26%, what would be the impact of this expense on Global’s earnings?

- How would it impact Global’s cash at the end of the year?

✔ In the end, accelerating depreciation cuts your tax bill and thereby increases cash flows. It lowers your earnings, but in a “non-cash” manner.

Depreciation decreases Pretax income by $1M. This also decreases your tax bill by $0.26M. On the statements of Cash Flows, we add the $1M of depreciation back in, so that the final incremental cash flows are exactly +$0.26M.

Income Statement and Statement of Cash Flows

- Recall that depreciation is not an actual cash outflow, even though it is treated as an expense, so the only effect on cash flow is through the reduction in taxes

- Global’s operating income, EBIT, and pretax income would fall by $1 million because of the $1 million in additional operating expense due to depreciation

- This $1 million decrease in pretax income would reduce Global’s tax bill by 26% ´ $1 million = $0.26 million

- Therefore, net income would fall by 1 - 0.26 = $0.74 million

- On the statement of cash flows, net income would fall by $0.74 million, but we would add back the additional depreciation of $1 million because it is not a cash expense

- Thus, cash from operating activities would rise by -0.74 + 1 = $0.26 million

- Thus, Global’s cash balance at the end of the year would increase by $0.26 million, the amount of the tax savings that resulted from the additional depreciation deduction

- The increase in cash balance comes completely from the reduction in taxes

- Because Global pays $0.26 million less in taxes even though its cash expenses have not increased, it has $0.26 million more in cash at the end of the year

Feedback? Email robmgmte2700@gmail.com 📧. Be sure to mention the page you are responding to.