In general, we don’t like ARR because it doesn’t respect the time value of money. Therefore, we won’t spend much time on it.

To some degree, this slide is here to remind us that it is important to account for the Time Value of Money.

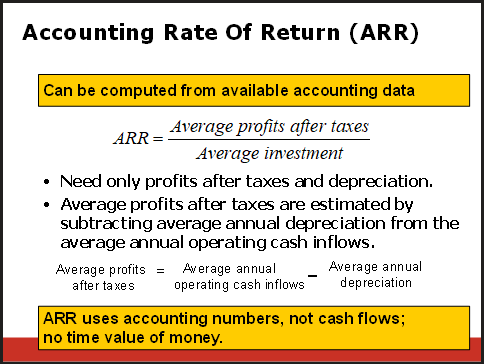

ARR comes down to two equations:

A R R = Average profits after taxes Average investment ARR=\frac{\text{Average profits after taxes}}{\text{Average investment}} A RR = Average investment Average profits after taxes Average profits after taxes = Average annual operating cash inflows − Average annual depreciation \text{Average profits after taxes}=\text{Average annual operating cash inflows} - \text{Average annual depreciation} Average profits after taxes = Average annual operating cash inflows − Average annual depreciation ❔ What was Apple’s ARR. You have the opportunity to lease “Apple” for 3 years for and annual cost of $233B per year. Assume that Apple’s annual operating cash inflows are $102,288 on average and Apple’s total annual depreciation is $11,148 on average.

✔ Click here to view answer Average Profits After Taxes = Av Ann Operating Cash Inflows − Av Ann Depreciation = 102 , 288 − 11 , 148 = 91 , 140 \text{Average Profits After Taxes} = \text{Av Ann Operating Cash Inflows} - \text{Av Ann Depreciation} = 102,288 - 11,148 = 91,140 Average Profits After Taxes = Av Ann Operating Cash Inflows − Av Ann Depreciation = 102 , 288 − 11 , 148 = 91 , 140

A R R = Avg Profit Aft Tax Avg Investment = 91 , 140 233 , 000 = 0.3912 ARR = \frac{\text{Avg Profit Aft Tax}}{\text{Avg Investment}} = \frac{91,140}{233,000} = 0.3912 A RR = Avg Investment Avg Profit Aft Tax = 233 , 000 91 , 140 = 0.3912