🔎 Why are i and c different?

The best way to answer this is to look at a little history.

The historical way to look at a bond: interest rate = coupon rate

Section titled “The historical way to look at a bond: interest rate = coupon rate”Historically, the coupon rate of a bond acted like an interest rate.

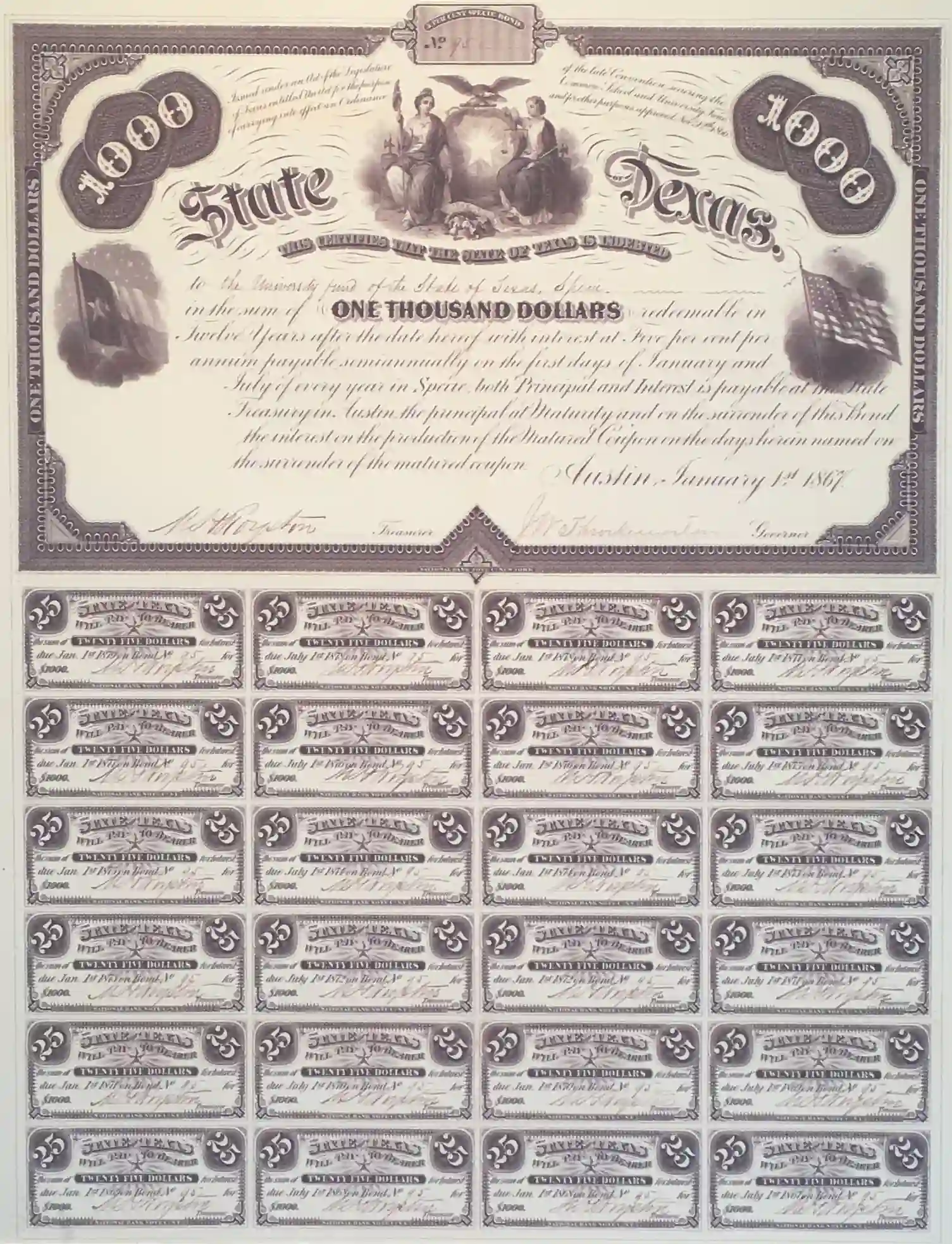

For example, you can read on the following bond that the borrower - the state of Texas - owes the investor $1000 and pays them a 5% of that as an interest payment every year. (Specifically, it pays the investor $25 twice a year.)

Text:

This certifies that the State of Texas is indebted to the University Fund of the State of Texas, Specie [specie=precious metal coinage] in the sum of ONE THOUSAND DOLLARS [F=$1000] redeemable in twelve years [T=12] after the date hereof with interest at Five percent per annum [c=5%] payable semiannually on the first days of January and July of every year in Specie, both principal and interest is payable at the State Treasury in Austin. The principal at maturity and on the surrender of this bond. the interest on the production of the matured coupon on the days herein named on the surrender of the matured coupon.

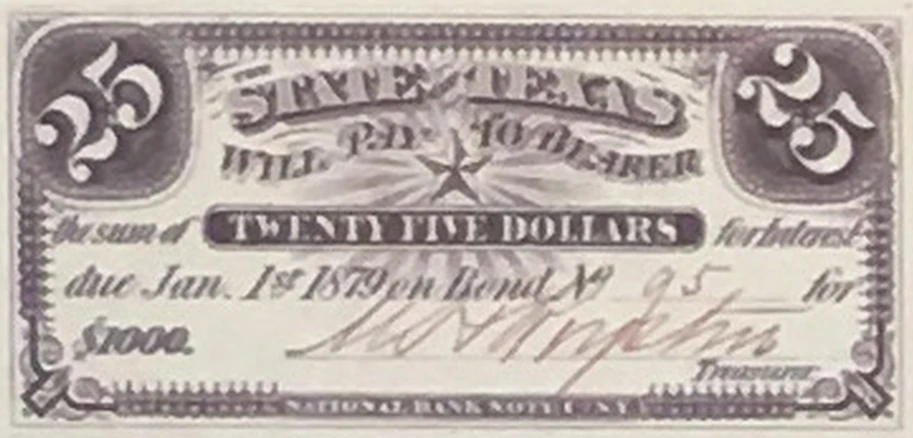

Here is a closeup of a coupon:

The text on the coupon is as follows:

The State of Texas will pay to the bearer the sum of TWENTY FIVE DOLLARS for interest due July 1st 1867 on bond no. 95 for $1000.

The new way: interest rate = the actual rate of return you receive (IRR)

Section titled “The new way: interest rate = the actual rate of return you receive (IRR)”Thinking of the interest rate as being the coupon rate works until the bond begins being re-sold.

Clearly, if you purchase the above bond for $500 instead of $1000, then the final return that you get will be higher than the 5% coupon rate. This is because you would be buying $1000 of debt, but paying far less than $1000 for it.

Likewise, if you purchase the above bond for $1500 instead of $1000, then the final return that you get will be less than the 5% coupon rate. This is because you would be buying $1000 of debt, but paying a very large premium. Overpaying for the debt will drag down your total return.

Clearly, the actual price that you pay will determine the return that you earn on the bond.

This is the heart of why we pay attention to YTM as the return of a bond and why we largely ignore the coupon rate of the bond.

YTM just uses our general tool of IRR to calculate the return on purchasing a bond and holding it to maturity. Remember that IRR can be used to calculate the return of any investment that you make. It is therefore very natural to consider the IRR you receive in you purchase a bond and hold it to maturity (YTM).

Note that if you purchase a bond for its face value and hold it to maturity, then your IRR will be equal to the coupon rate. We already know this because we know that when , . Therefore, the historical idea of thinking of the interest rate as the coupon rate is still true! It still applies if we purchase the bond for its face value. It’s only when we purchase the bond at a discount (ie a discount bond) or at a premium (ie a premium bond) that the Yield to Maturity will differ from the coupon rate. Here is a summary table:

| ⇔ | ⇔ | “Discount Bond” | ||

| ⇔ | ⇔ | “Par Bond” | ||

| ⇔ | ⇔ | “Premium Bond” |

Many bonds are bought and sold in the secondary market every day. In fact, the secondary market for bonds is many times more active than the stock market.

Feedback? Email robmgmte2700@gmail.com 📧. Be sure to mention the page you are responding to.