🙋 Student Q&A (Lecture 10)

Click here to learn about timestamps and my process for answering questions. Section agendas can be found here. Email office hour questions to robmgmte2700@gmail.com. PS1Q2=“Question 2 of Problem Set 1”

📅 Questions covered Saturday, Apr 18

Section titled “📅 Questions covered , Apr 18”No questions emailed.

📅 Questions covered Monday, Apr 20

Section titled “📅 Questions covered , Apr 20”🕣 Started around 8:00 -8:15ish

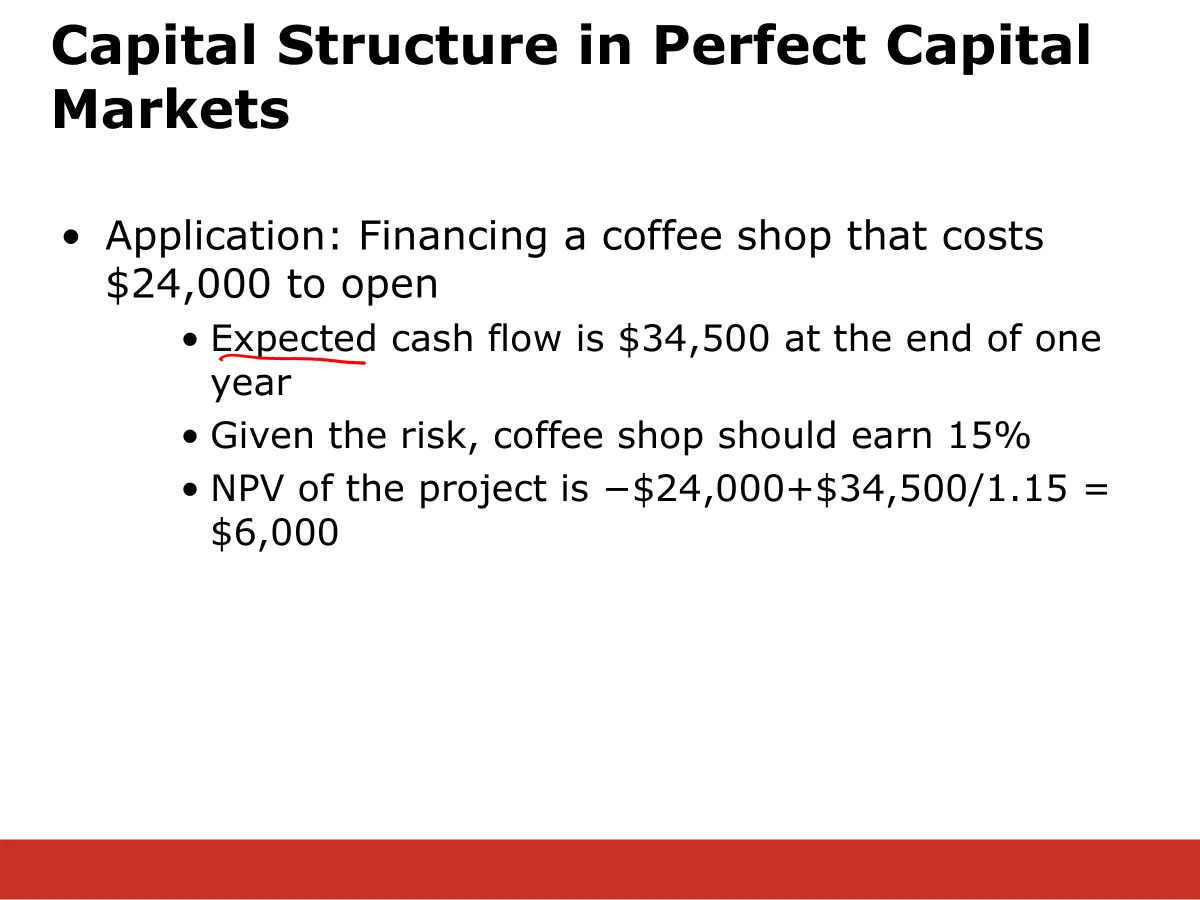

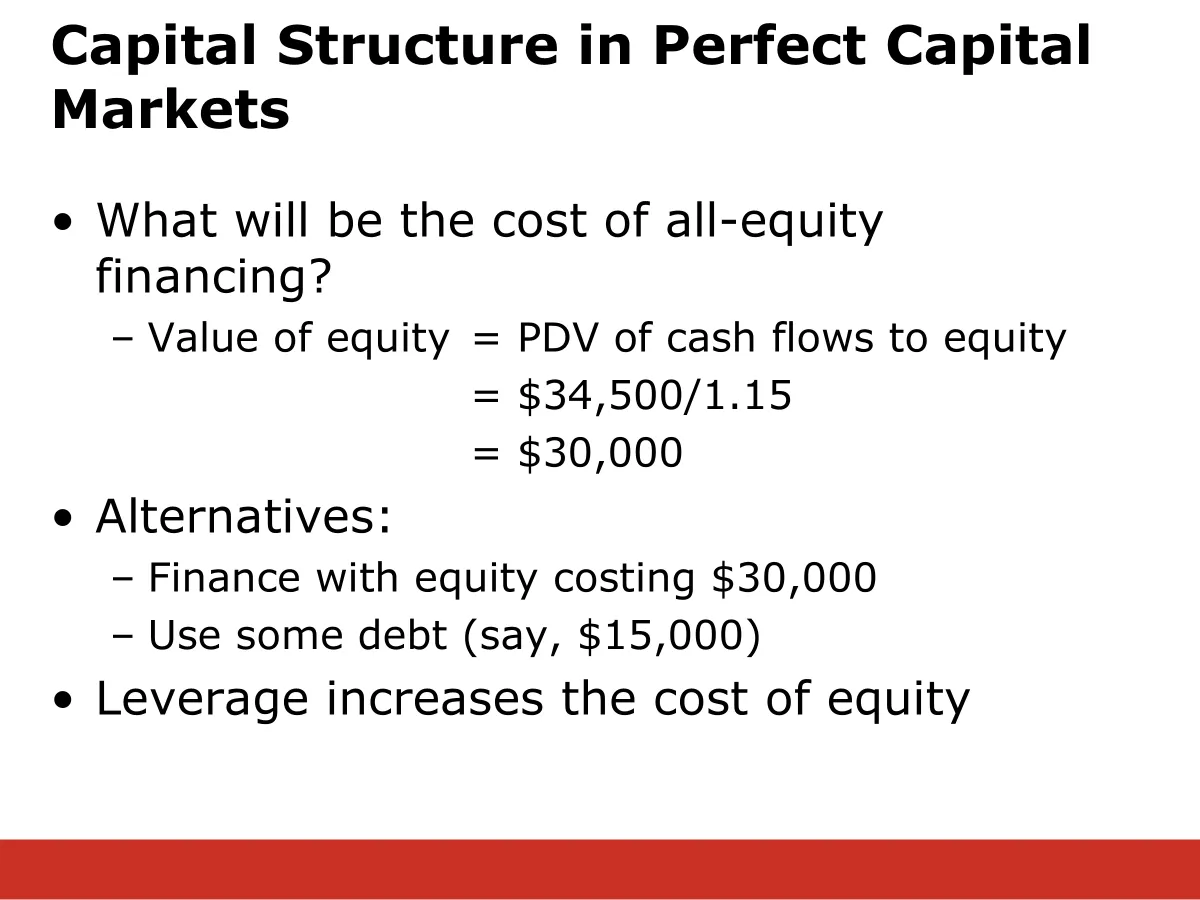

❔ Slides starting at 11. Where does the $24K come from? Where does the $30K come from?

✔

🕣 8:40pm

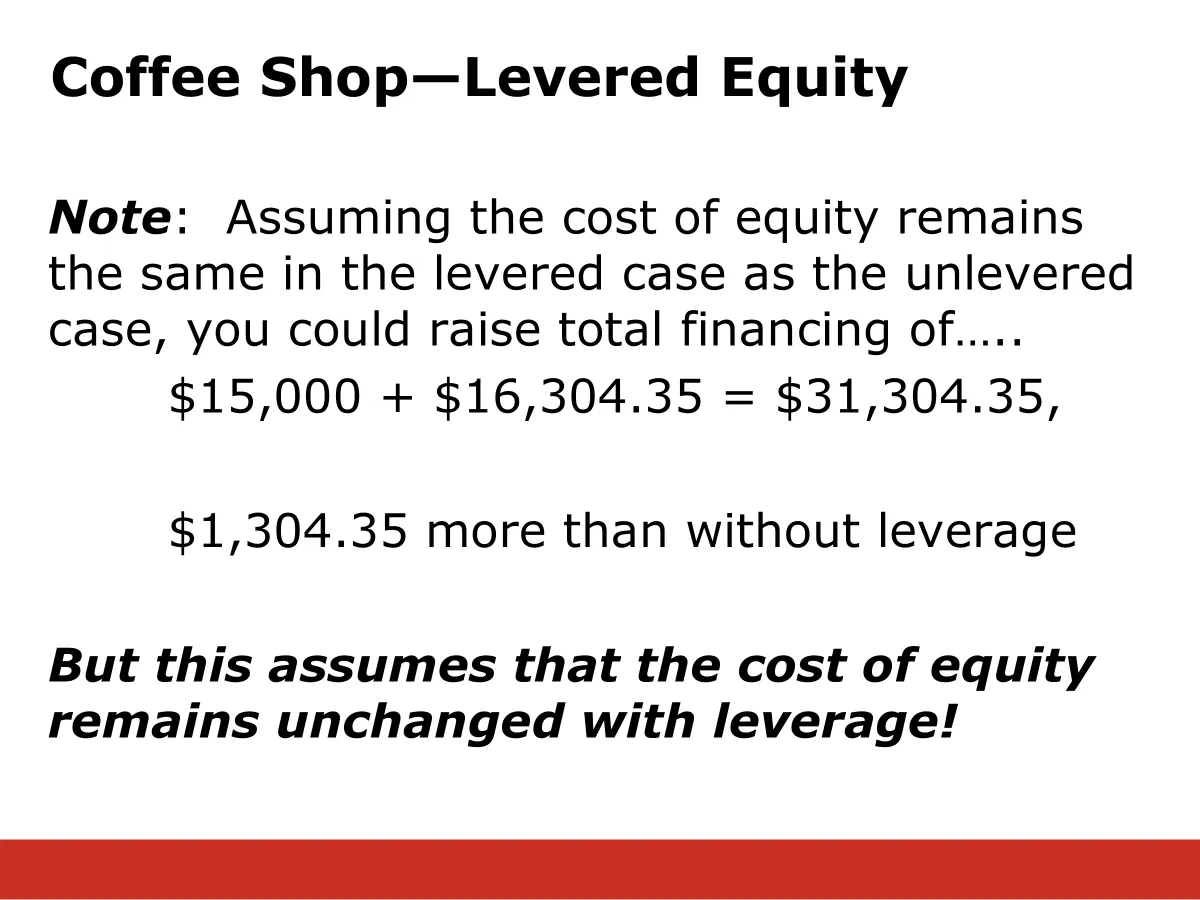

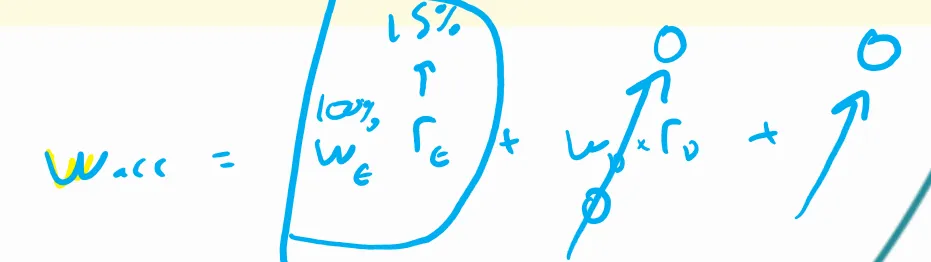

❔ Also slide 16. How do we find the cost of capital for levered equity?

✔ Pulled it together at 8:54pm

🕣 9:03pm

❔ Pretax WACC practice problems. Slides 37-44

✔

🕣 9:12pm

❔ Regarding seasoned equity offerings and doing a cash raise versus a rights offering, it seems to me like the former poses dilution risk via offering the equity to new investors, whereas the latter does not dilute assuming all existing shareholders exercise their rights. ❔ Also, in the case of the rights offering, it would seem this would often be done in distress situations before offering the equity to outside investors. Is my line of thinking sound here?

✔ Yes on both. Often you will do a rights offering if the firm is in enough distress that it can’t raise money from the regular equity markets.

🕣 9:13pm

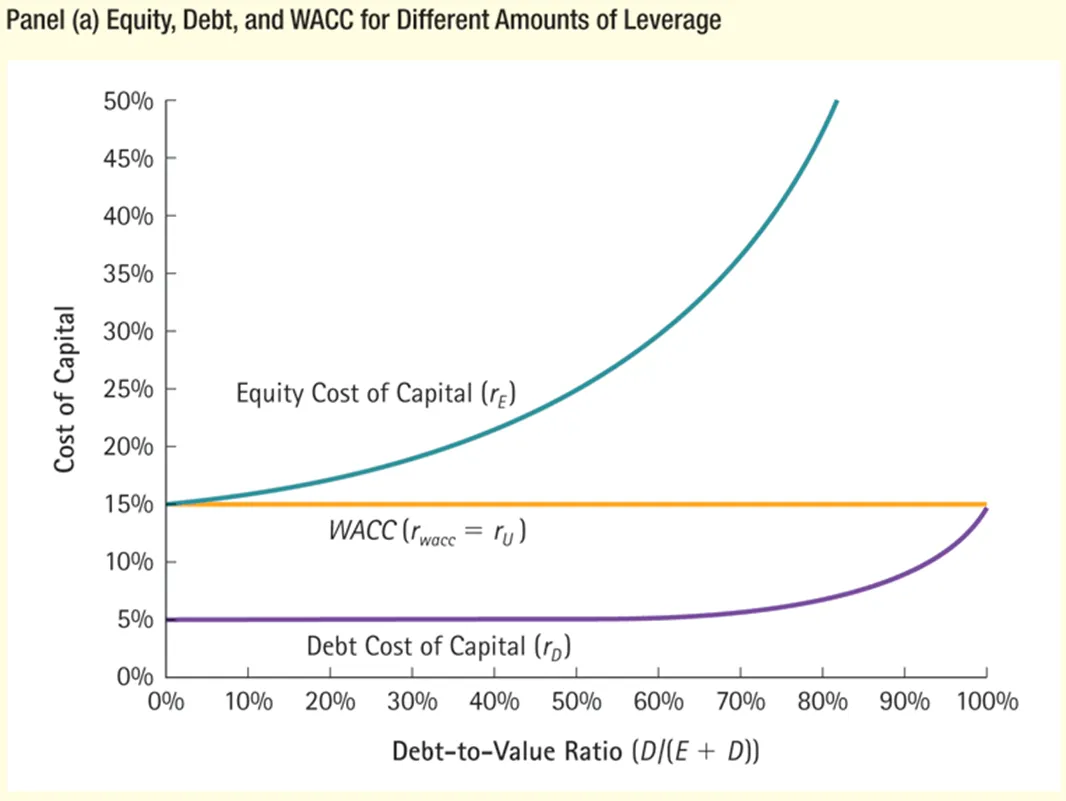

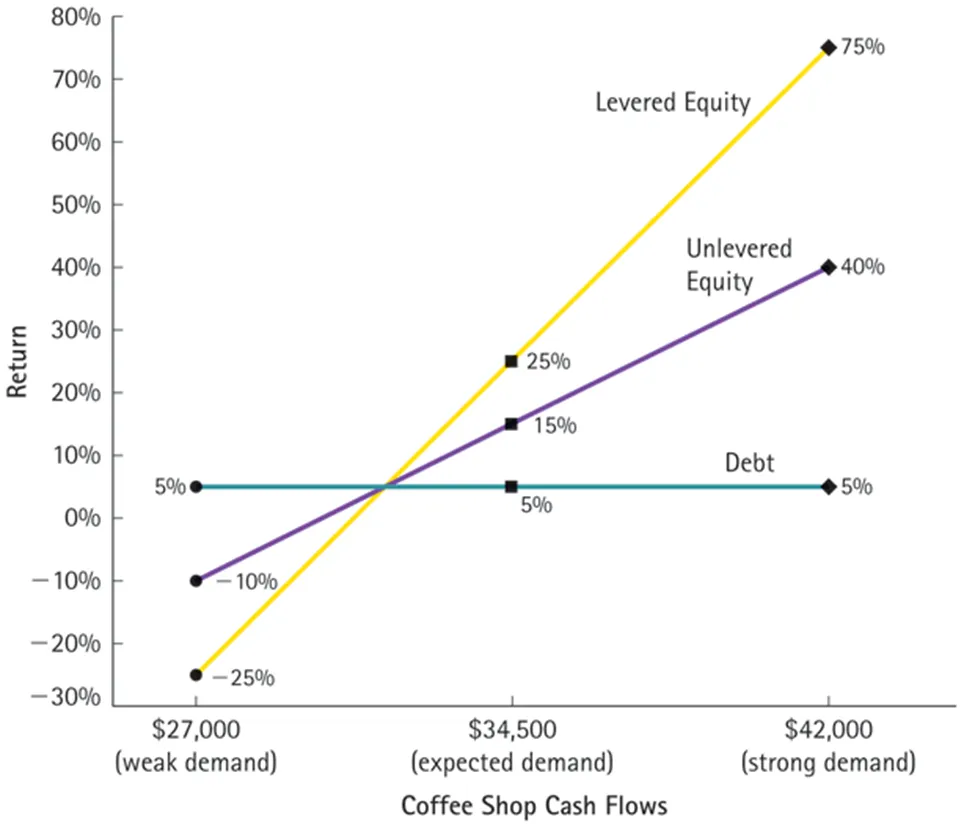

❔ - I’ve attached an example regarding the MM propositions, and was thinking about when leverage works in a company’s favor and when it doesn’t. Basically, when return on assets <> return on debt, you end up with negative and positive leverage,illustrating that debt magnifies returns and the sword does indeed cut both ways. If you have a moment, could you please tell me if you agree with my analysis.

✔

🕣 9:17pm

❔ For question 4 on the problem set, do “case (a)” and “case (b)” refer to the weak and strong outcomes, respectively, or is it referring back to steps a and b in the problem?

✔ It means parts a and b from the the problem, not the weak and strong outcomes.

Feedback? Email robmgmte2700@gmail.com 📧. Be sure to mention the page you are responding to.