🙋 Student Q&A (Lecture 13)

Click here to learn about timestamps and my process for answering questions. Section agendas can be found here. Email office hour questions to robmgmte2700@gmail.com. PS1Q2=“Question 2 of Problem Set 1”

📅 Questions covered Saturday, May 9

Section titled “📅 Questions covered , May 9”🕣 At start

❔ Could we please go over the following finance problem together? I would like to use Excel to help solve this more efficiently.

Problem Details:

- Acquiring Company: Earnings per share of $4.00, 1 million shares outstanding, and a current share price of $40.00.

- TargetCo: Earnings per share of $2.00, 1 million shares outstanding, and a price per share of $25.00.

- Transaction Terms: The acquisition will be paid for by issuing new shares. There are no expected synergies. The exchange ratio is set at a 20% premium based on current pre-announcement prices.

- Market Reaction: On announcement, the target price will rise and the acquiring company’s price will fall to reflect the premium paid without synergies.

I am looking to calculate the following: a. The price per share of the combined corporation immediately after the merger. $37.14 b. The price of our company immediately after the announcement. $37.14 c. The price of TargetCo immediately after the announcement. d. The actual premium our company will pay.

This is Problem Set 10 number 7

Please let me know when you might be available to walk through this and set up the Excel model.

🕣 2:09pm

❔ Problem Set 8, specifically number 3 . Could we please review these questions together and walk through the solutions using Excel?

🕣 2:31pm

❔ Problem Set 8, specifically number 6. Could we please review these questions together and walk through the solutions using Excel?

🕣 2:41pm

❔ NPV Complex Scenarios - Converting to timeline

✔ You can find more examples in the problem sets and in the slides. However, bite sized questions will tend to have simpler setups than the slides and the problem sets on average, so it shouldn’t be your main priority.

I’m not sure I understand what you mean here, so I’d need a bit more context. Are you talking about examples, or is this just a straightforward NPV problem where you need to calculate free cash flows? A couple of the problem set questions require calculating free cash flows, and those are much more complicated, but byte-sized problems are less likely to be that sophisticated.

A lot of this is about covering the core concepts quickly. I love that you’re asking this question. It’s a nice, hard question.

This isn’t easy, but it ties together a lot of the core concepts you want to know, so it will give you a lot of practice. It ended up being a hard one.

Based on https://2700.robmunger.com/l5/3yearexample/

✏️ Consider a two-year project that takes one year to set up. During the setup year, you will have $3 million in expenses. You will also have $20 million in capital expenditures, which will go toward a new data center. This capex is due at the very start of the project (immediately).

The data center will only be usable for two years. It will become usable exactly one year from now, after it is built and installed. It will remain usable for two years, reaching the end of its usable life exactly three years from now. During that time, there will be $5 million in annual operational expenses. In addition to the $5 million in annual operational expenses, you will need $3 million in additional working capital each year for the two years the data center is operational.

There will also be revenue. Over the two years the data center is operational, revenue will be $20 million per year. Given the riskiness of this project, your cost of capital is 15%. Tax expense is 20%.

Is this a good project to invest in? What is this NPV?

🕣

❔ L3 (PS1) EBIT = Operating Income +/- Other income

✔

🕣

❔ Stock Valuation for WACC

r = rF + β(Erm - rF)

✔

📅 Questions covered Monday, May 11

Section titled “📅 Questions covered , May 11”🕣 7:50pm

❔ One thing that is still difficult for me to understand is the logic behind the value per share in SEOs. I think it would help me if you could walk us through slide 95 in lecture 8 (March 31), especially focusing on the 5 rights for two shares part. It makes sense reading it, but it would be hard for me to remember on the exam. Maybe you could just explain the reasoning in a way that is more intuitive.

✔

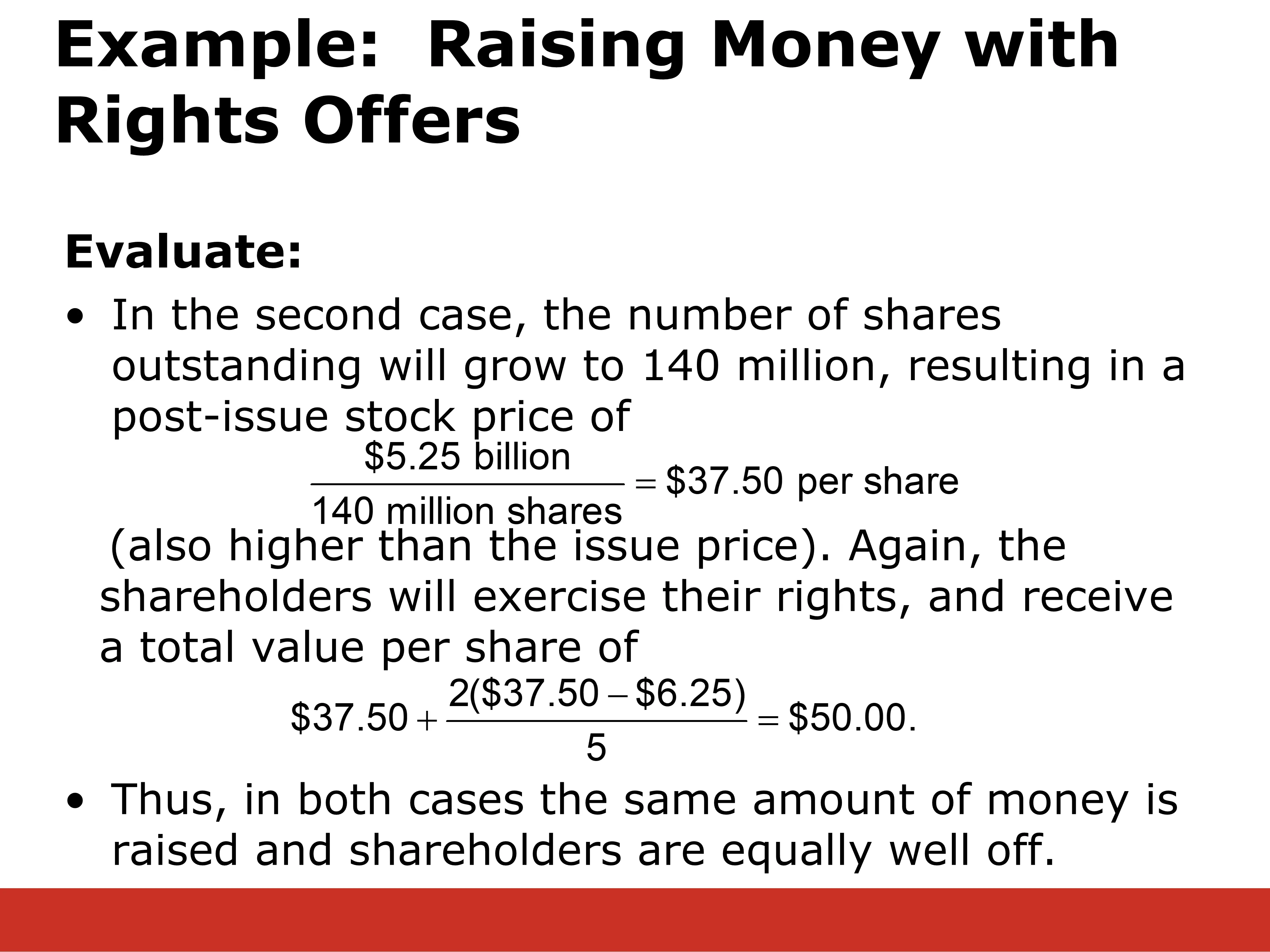

- You are the CFO of a company that has a market capitalization of $5 billion. The firm has 100 million shares outstanding, so the shares are trading at $50 per share.

- You need to raise $250 million and have announced a rights issue. Each existing shareholder is sent one right for every share he or she owns.

- You will require either two rights to purchase one share at a price of $5 per share, or five rights to purchase two new shares at a price of $6.25 per share.

Option 1: 2 shares/rights → package → 1 share @$5

- Money raised:

- 100m shares/2shares per package = 50m packages.

- 50m packages × 1 share purchased per package = 50m new shares purchased @$5

- 50m × $5 = $250M

- How do shareholders do?

- How much is a share worth? Company was worth MC=$5B and it raised $250M, so it is now worth $5.25B. There are now 100M + 50M = 150M total shares. We back the share price out of the market cap: P = MC/#Shares = 5.25B/150M = $35.

- How much value did the shareholders get by purchasing a share at a discount? They paid $5 for a share that is now worth $35, so they got a $30 discount for each “package.” Since there two rights are required to get this discount (ie 2 shares per package), that means that owning a share entitles an investor to a discount of $30/2shares = $15 per share. In other words, the rights offering is giving people a value of $15 per share.

- What is the total value that shareholders have after all of this has happened? They had an individual share worth $35. They received the rights offering, which gave them a $15 discount per share, so in total they were left with $50. That is exactly what they started with. This illustrates, once again, that, in some ways, you cannot create value through financial engineering.

- This sounds very pessimistic until you realize the company actually needed the money, and this is how it raised it. If the company is facing distress costs, this money could help it avoid those costs and create shareholder value, so it is not a bad thing, even though it did not help shareholders in this calculation. That is only because we have not explicitly modeled the benefits of giving the company the cash. We said the company’s market cap after the cash infusion was $5.25 billion. If it really needed that $250 million, it might have actually raised the value of the company. Option 2: 5 shares/rights → package → 2 shares @$6.25

- Money Raised:

- 100m shares/5shares per package = 20m packages.

- 20m packages × 2 share purchased per package = 40m new shares purchased @$6.25

- 40m × $6.25 = $250M

- How do shareholders do?

- How much is a share worth? Company was worth MC=$5B and it raised $250M, so it is now worth $5.25B. There are now 100M + 40M = 140M total shares. We back the share price out of the market cap: P = MC/#Shares = 5.25B/140M = $37.50.

- How much value did the shareholders get by purchasing a share at a discount? They paid $6.25 for a pair of share that is now worth $37.50×2 = $75, so they got a $75-$12.50 = $62.50 discount for each “package.” Since there 5 rights are required to get this discount (ie 5 shares per package), that means that owning a share entitles an investor to a discount of $62.50/5shares = $12.50 per share. In other words, the rights offering is giving people a value of $12.50 per share.

- What is the total value that shareholders have after all of this has happened? They had an individual share worth $37.50. They received the rights offering, which gave them a $12.50 discount per share, so in total they were left with $50. That is exactly what they started with. This illustrates, once again, that, in some ways, you cannot create value through financial engineering. However, see the “this sounds pessimistic” bullet point above for how it could benefit people.

🕣

❔ PS10 Q3

✔

🕣

❔ Would it be possible for us to go over the auction IPO on Rob’s site? I see that it is covered in Week 8.

Additionally, I would like to review a specific question from the Week 8 materials regarding the calculation of ownership value. The example provided is:

If you own 15% of a company that has a post-money valuation of $20M, the value of your stake is $3M based on the following formulas:

Formula #1: % ownership × valuation of firm = valuation of your stake in firm (15% × $20M = $3M)

Formula #2: valuation of your stake in firm = # Shares You Own × $ Price Per Share

Returning to that original example, I would like to go over the value of the stake in the firm to ensure I have a full understanding of the calculation.

During the math part in week 8 you said this but it’s not clicking to me how you got there 3.57% y + 3.57*900M = y - 3.57%y = 96.43% y

✔

🕣 8:40pm

❔ I’ve now worked enough M&A examples to arrive at the following conclusions:

No premium or synergies = the acquirer’s existing shareholders are neither better or worse off;

Premium, but no synergy = the acquirer’s existing shareholders are worse off;

Synergies > premium = the acquirer’s existing shareholders are better off; and

Synergies < premium = the acquirer’s existing shareholders are worse off.

✔ Excellent points! It’s wonderful how our model can illustrate some key insights into what makes a merger that adds to shareholder value versus what makes a merger that detracts from shareholder value.

🕣 8:57pm

❔ Are we also responsible to know how to do these questions with a combination of cash and shares? I created some examples to also work the math under this scenario just in case.

✔ You’re only responsible for what Bruce covered in class. There’s a small chance he might slightly extrapolate from what was covered, but I don’t expect that to happen.

In my opinion, the challenge of this exam isn’t coming up with novel ideas. It’s executing the core skills and concepts quickly, so you need to know them well.

🕣 9pm

❔

In addition, I was giving more thought to D* and what it actually means and how it is derived. I was hung up thinking it occurred where the PV of Interest Tax Shield = PV of Financial Distress Costs, but I think it is actually found on the margin. Meaning, and like in Econ 1010, D* occurs not where the PVs equate, but rather where the marginal tax benefit from interest = marginal cost of financial distress. Is my line of thinking out to lunch here?

✔ I’m not sure I fully understand the question. Financial distress costs refer to situations where a firm may not be able to pay what it owes and could potentially go bankrupt.

For a parallel in banking, most of what we’re looking at in financial crises and banking problems is either solvency (can the firm eventually pay back all its debts, and what’s its net worth?) or liquidity. Liquidity is different. Distressed costs are related to liquidity.

A firm can be very valuable in the future (for example, an AI company that will be worth $1 trillion someday), but if it can’t pay bills that are due today, it could be gone. If it’s gone, all that potential value could evaporate as creditors, lawyers, and others fight over what’s left. Most of a firm’s value comes from its people, IP, and physical assets working together to create value and generate free cash flow.

If a liquidity problem leads to bankruptcy, there can be a lot of distressed costs. It’s not a bad time to review exactly what those costs are.

Are we in Lecture 10, or are we in Lecture 11?

In the chat, a student mentions that this is similar to Silicon Valley Bank. Yeah, exactly. It’s all about liquidity. Once you have that situation, a bank is just a big bundle of liabilities (debt obligations). That’s what a deposit is: someone’s promise to pay you back.

People tried to withdraw their deposits, and it had to close its doors. I’d have to review the timeline exactly of how it went, but that’s kind of the liquidity story.

That’s why I also focus on real high-net-worth clientele. When people were withdrawing, it was significant, large amounts. One of the issues when you focus on high-net-worth individuals is that they’re not FDIC insured. If they’re worried, they’re really worried. If a regular Joe Schmoe’s bank is in trouble, they’re not really worried because they probably don’t have more than $250,000 in any given account at a given institution. If you’ve got $5 million in your checking or savings account and it’s only insured for $250,000, you get pretty nervous and you’re going to pull your money when you need to.

A big issue is that they had bought a lot of 10-year Treasuries. We think of Treasuries as being relatively low-risk, but they still have interest-rate risk. When inflation hit, interest rates started spiking because the Fed lifted them, and the value of those bonds really plummeted. Once they had to mark those bonds to market, they suddenly looked close to insolvent, and that kicked off some of the things Ian was just discussing. It kicked off the liquidity issue.

All of that stuff can happen even if it’s got this great business model. If it didn’t have the liquidity crisis, maybe it was going to go on to be a trillion-dollar bank. Who knows, but if you can’t pay your bills today, you’re still going to sink today.

🕣

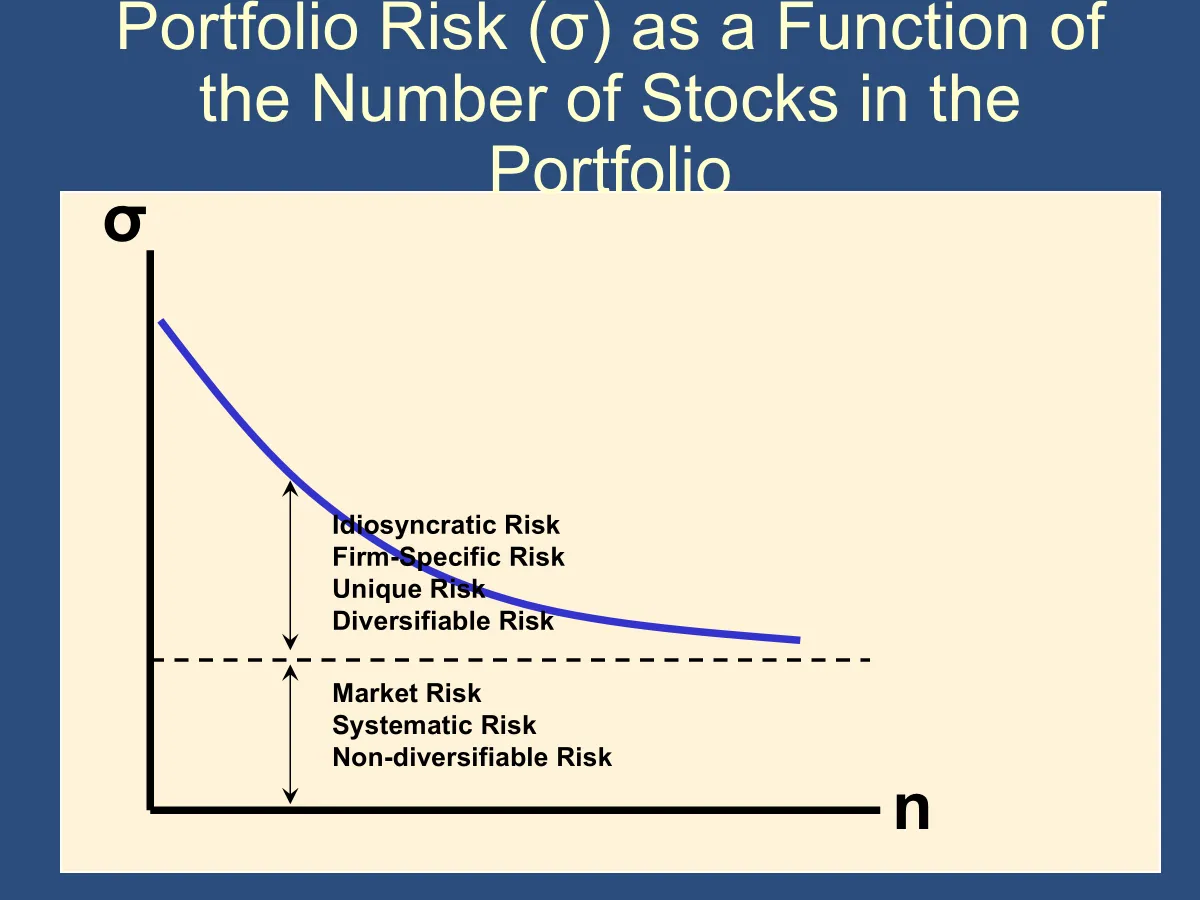

❔ Beta - is it market risk, firm specific risk, or systemic risk.

✔ Beta is a measure of the systematic non-diversifiable or market risk of a given investment or portfolio of investments.

🕣 9:13pm

❔ Can you explain the following and do an example.

✔

✏️ Suppose a firm pays a $2 annual dividend, its current stock price is $25 per share, and the dividend is expected to grow at about 3% per year. What return would you expect on that stock? Given that, what would be an appropriate cost of equity for the stock?

✔ If all that you received from holding this stock was the dividend, it would be paying you a return, just based on the steady stream of dividends, that you could quantify.

What is the percentage return that you receive based solely on the current dividend?

You have invested $25 and you get an annual income of $2. You get a return of 2/25 = 8% per year.

The number we just calculated is called the dividend yield. As shown in the screenshot above, it’s calculated by dividing the dividend by the current price.

The dividend yield doesn’t account for the fact that the company is growing. Since the company is growing, its dividend will grow, and that means its share price should grow too. If the dividend is increasing by 3% per year, the share price should be growing at 3% per year as well. That means we should add 3% to the return we’re getting from this stock.

Therefore the total return is 8% (dividend yield) + 3% (dividend growth rate) = 11%.

This is the idea captured in the screenshot:

Return on the stock = 2/25 + 3% = 11%.

CDGM: Return on equity = dividend yield + dividend growth rate = dividend/price + dividend growth rate. ✅

One of the nice things about the constant dividend growth model is that many problems will follow a similar pattern. You will be given a problem, and within it, you will find the information you need to calculate the cost of equity. You just have to plug that information into the constant dividend growth model to solve for the cost of equity.

Conceivably, there could be another type of problem in which he asks for a different number in that same formula. Here’s an example:

🙋 This is used for companies solely that still pay dividends right? So, it is less popular of a formula present time?

✔ Yes. Because dividends have become less popular and make up a smaller share of how companies return cash to shareholders, Bruce definitely doesn’t like it. That’s the main reason he doesn’t like this formula. I think Ryan mentioned that earlier and made a joke about it.

There are other ways firms can return earnings to shareholders, including share buybacks. You can replace dividends with dividends plus buybacks, so it could be total return to shareholders.

🕣

❔ Please finish the Data Center Question.

✔

Feedback? Email robmgmte2700@gmail.com 📧. Be sure to mention the page you are responding to.