🙋♀️ Interpreting Question 4 (PS5)

This page builds on insights from: 🔎 The Corporate Finance Perspective

In a multipart question like this, it can be easy to lose sight of the big picture of the question. However, the big picture is laid out in the original prompt for the question:

“Because all of the cash flows from the assets must go either to the debt or the equity, if you hold a portfolio of the debt and equity in the same proportions as the firm’s capital structure, your portfolio should earn exactly the expected return on the firm’s assets. Show that a portfolio invested in the firm’s debt and in its equity will have the same expected return as the assets of the firm. That is, show that the firm’s WACC is the same as the expected return on its assets.”

The big picture of this question is to show that the first line (expected return on Assets) equals the last line (expected return on portfolio):

❔ What does the word “expected” mean? In particular, what is “expected return?”

✔ Whenever you see the word expected, you should calculate an expected value. An expected value is a weighted average where the weights are the probabilities of the outcome happening. We use a capital E, “E(),” to represent expected value.

- Expected Value (EV)

- = Probability of Outcome 1 × Value of Outcome 1

- + Probability of Outcome 2 × Value of Outcome 2

- + Probability of Outcome 3 × Value of Outcome 3

- + …

- + Probability of Outcome N × Value of Outcome N

For example:

✏️ Suppose a given stock has a 40% chance of having a return of 7%, but a 60% chance of having a return of 16%. What is its “expected” return?

✔ Click here to view answer

Expected Return = Expected Value of the Return

You will need to use this formula twice in this problem to calculate out “expected return.”

Equally likely means “50/50”

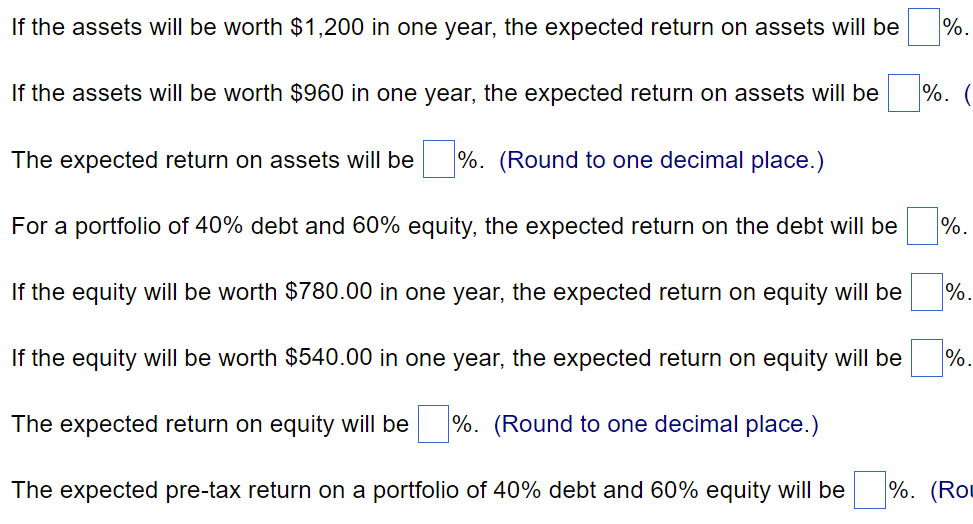

❔ What is the return on an asset such as the assets of the firm, the debt of the firm, or the equity of firm? (In other words, how do I calculate the “return on assets,” “return on debt,” “return on equity,” and “return on portfolio.”) See the circled quantities:

✔ Let’s do an example…

✏️ Suppose an asset has a market value of $200 today. If it’s return rises to $230 in one year, what is the return on this asset?

✔ Click here to view answer

You may know this formula as the “growth rate” formula. It’s a special case of the “holding period return” formula, which is, in turn, just calculating the Internal Rate of Return when you hold an asset for one period.

You must use a formula like this to calculate the circled quantities to the right. (For the last one, it’s easier to use the formula below.) Note: it’s impossible to use the formulas from the earlier chapters about “Return on Equity” “Return on Assets” because we can’t calculate the Net Income of the firm. In particular, we know nothing about the tax rate.

You might have an objection to this:

🙋♂️ But wait, suppose I’ve held the asset for years, so I didn’t buy the asset today. Suppose I didn’t sell the asset next year, either. How can you claim that my value is $200 today and $230 next year. That’s just the market value; it’s not my value. How can you say that I received a 15% return?

✔ There are complicated reasons for this assumption.

In general, we will take the value of something to be its market value.

❔ How do I calculate the return on a portfolio?

✔ To calculate the return on a portfolio, just calculate the weighted average of the returns on the assets in the portfolio. For example, suppose an endowment has a portfolio that is 30% in hedge funds/PE that is earning 15%, 60% in public assets that are earning 13%, and 10% in cash that is earning 0%. The return on the portfolio is

Let’s put this all together in a larger practice problem:

✏️ Consider a company that is funded by debt and equity. It develops and markets an app for mobile phones in a rapidly growing sector. The debt has a market value of $11M and equity has a market value of $9M. We will say that the assets are therefore worth $11M + $9M = $20M. See this: What is Enterprise Value?

The debt has a yield to maturity of 10%. The assets of the firm may rise or fall. If the firm achieves a dominant position in its industry, the assets will be worth $30M. If not, the assets will be worth only $15M. The probability of achieving a dominant position is 60%.

What are the expected returns on equity, debt, and assets? Verify that the expected return on a portfolio of the debt and equity of the firm has the same return as the assets themselves have. You may assume that the portfolio holds the debt and equity in the same ratios that the firm issues them.

✔ Click here to view answer

EXPECTED RETURN ON ASSETS:

Section titled “EXPECTED RETURN ON ASSETS:”Recall that:

- If the firm becomes dominant, the (expected) return on the assets will be:

- If the firm doesn’t become dominant, the return on assets will be:

Let’s put this a table:

| Return | Probability | |

|---|---|---|

| Good Outcome | 50% | 60% |

| Bad Outcome | -25% | 40% |

The expected return on assets is: (using the expected value formula)

EXPECTED RETURN ON DEBT:

Section titled “EXPECTED RETURN ON DEBT:”The debt is currently worth $11M. The yield to maturity of the debt is 10%, so if the bonds do not default, the return on the debt should also be 10%.

But what if the debt defaults? We will assume in this class that debt will never default if the assets of the firm are worth far more than the debt payments to be made. In this case, the assets of the firm will either be worth $15M or $30M. Their total debt payments are . Either way, they will have enough assets to pay back their debt. Therefore, the return on debt is 10%.

EXPECTED RETURN ON EQUITY:

Section titled “EXPECTED RETURN ON EQUITY:”Suppose that the company achieves the dominant position. The assets are worth $30M. In this case, the debt will be paid off. It was worth $11M, but it has appreciated by 10%, so the debt (and any cash payments from the debt) are together worth .

Equity is a residual claimant, in that they own all of the assets after the debt has been paid off. If the Assets are worth $30M and the debt payments are $12.1M, then the equity is worth: if the company achieves market dominance. Because the initial value of the equity was $9M, the return on equity is if they achieve market dominance.

Suppose the company doesn’t achieve the dominant position. Then, based on the residual claimants approach, the equity will be worth . This is because the company is worth $15M, but is weighed down by $12.1M of debt, so there is only $2.9M left over for the “residual claimants:” the equity holders. (Equity holders are the most junior claims on the assets of the firm.) In this case, the return on equity is pretty terrible:

Putting this together, the expected return on equity can be calculated from the following table:

| Return | Probability | |

|---|---|---|

| Good Outcome | 98.89% | 60% |

| Bad Outcome | -67.78% | 40% |

EXPECTED RETURN ON THE PORTFOLIO:

Section titled “EXPECTED RETURN ON THE PORTFOLIO:”Let’s consider a portfolio that holds debt and equity in the same proportions as the firm’s capital structure. The company has $11M of debt financing (market value) and $9M of equity financing (market value), so its assets have a market value of $20M. Therefore, it is debt financed and equity financed.

55% of our portfolio gets the debt return of 10% and 45% of our portfolio gets the equity return of 32.22%. Therefore, our portfolio return is expected to be:

or approximately 20%.

Therefore, we have “[Verified] that the expected return on a portfolio of the debt and equity of the firm has the same return as the assets themselves have.”

🙋The question states the future values of equity as $780 and $540. Where the heck did it get these numbers from?

✔ The “residual claimant” approach

Because equity holders are always the residual claimants on the assets of the firm, we can often calculate the value of equity by subtracting the value of debt from the value of the assets:

[it’s just the accounting equation.]

PLEASE NOTE THAT I’M EXPLAINING WHERE THE NUMBERS IN THE QUESTION CAME FROM. THIS IS NOT THE ANSWER TO THE QUESTION. I’m just helping with question interpretation.

We can apply this logic to the problem set question to see where the equity values come from…

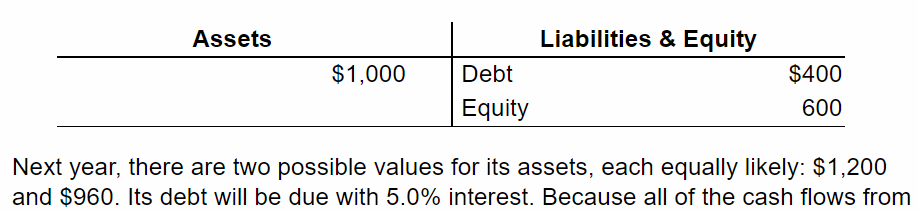

But how much will be owed on the debt next year?

The debt is worth $400 now. It will return 5%. Therefore, it will be worth .

If the assets are worth $1200 and the debt is worth $420, then if equity is a residual claimant on the assets, then it makes sense that equity would be worth .

Likewise, if assets are $960 and debt is still $420 (“fixed” income), then equity is worth .

Now we see where these two values come from:

I emphasize this because it helps you understand some later lectures. There are deep connections between this problem and the capital structure/Modigliani and Miller Lecture.

Feedback? Email robmgmte2700@gmail.com 📧. Be sure to mention the page you are responding to.