👨🏫 Notes

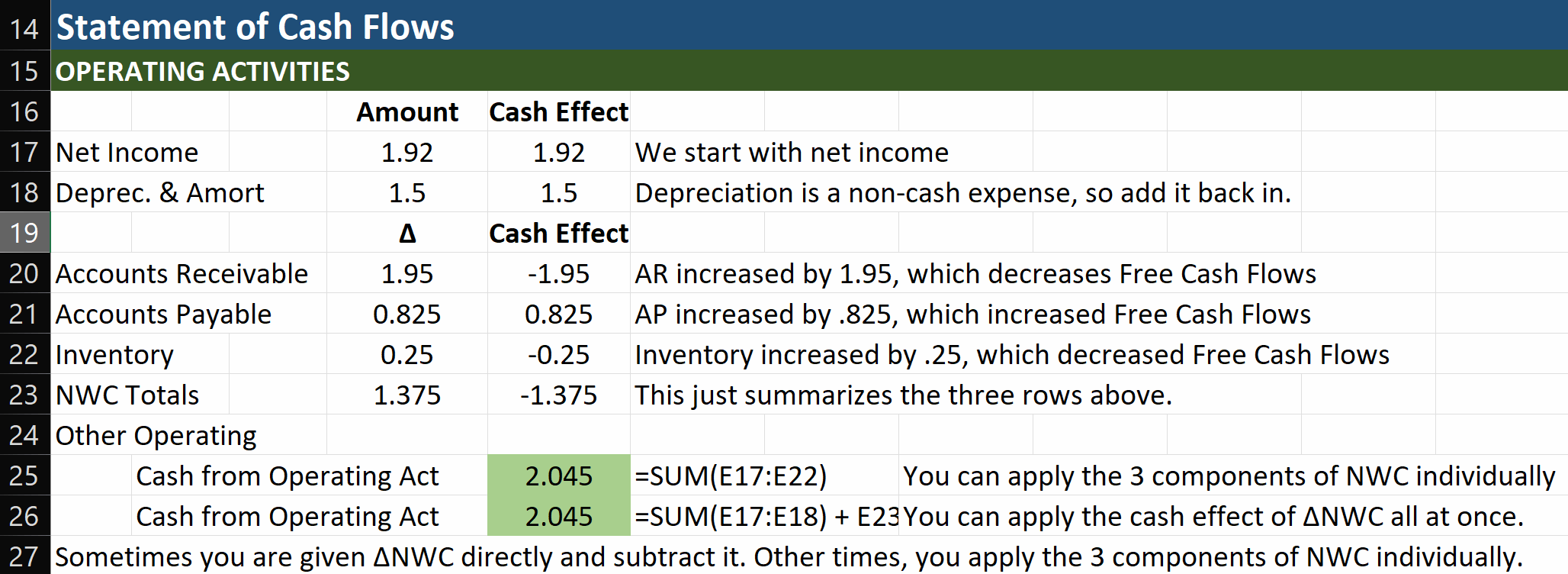

Statement of Cash Flows

The statement of cash flows is divided into three sections which roughly correspond to the three major jobs of the financial manager:

- Operating activities

- Investment activities

- Financing activities

Statement of Cash Flows: Operating Activities

Depreciation:

- We also add depreciation to net income, since it is not a cash outflow

Accounts receivable:

- Adjust the cash flows by deducting the increases in accounts receivable

- This increase represents additional lending by the firm to its customers and it reduces the cash available to the firm

Accounts payable:

- Similarly, we add increases in accounts payable

- Accounts payable represents borrowing by the firm from its suppliers

- This borrowing increases the cash available to the firm

Inventory:

- Finally, we deduct increases to inventory

- Increases to inventory are not recorded as an expense and do not contribute to net income

- However, the cost of increasing inventory is a cash outflow for the firm and must be deducted on the statement of cash flows.

Statement of Cash Flows: Investment and Financing Activities

Investment Activity

- Subtract the actual capital expenditure that the firm made

- Also deduct other assets purchased or investments made by the firm, such as acquisitions

Financing Activity

- The last section of the statement of cash flows shows the cash flows from financing activities

- Subtract Dividends paid

- Add cash received from sale of stock

- Subtract cash spent repurchasing your own stock

- Add changes to short-term and long-term borrowing

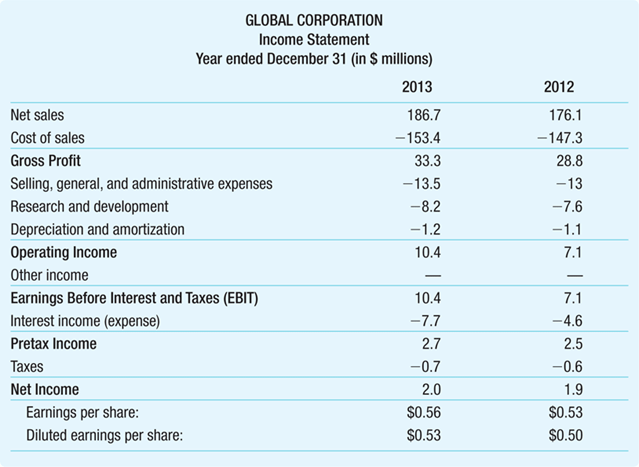

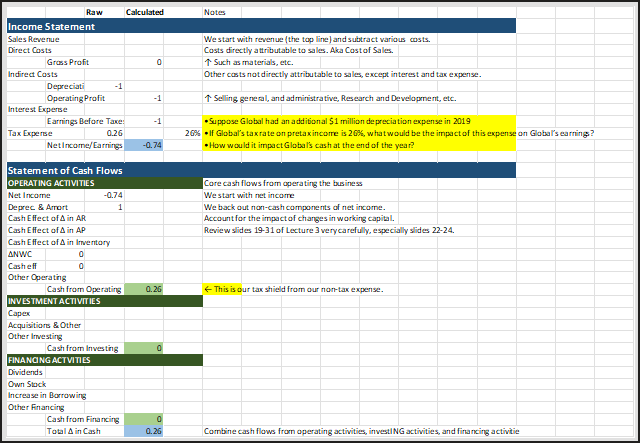

✏️ The Impact of Depreciation on Cash Flow

- Suppose Global had an additional $1 million depreciation expense in 2019

- If Global’s tax rate on pretax income is 26%, what would be the impact of this expense on Global’s earnings?

- How would it impact Global’s cash at the end of the year? ✔ In the end, accelerating depreciation cuts your tax bill and thereby increases cash flows. It lowers your earnings, but in a “non-cash” manner.

Depreciation decreases Pretax income by $1M. This also decreases your tax bill by $0.26M. On the statements of Cash Flows, we add the $1M of depreciation back in, so that the final incremental cash flows are exactly +$0.26M.

Income Statement and Statement of Cash Flows

- Recall that depreciation is not an actual cash outflow, even though it is treated as an expense, so the only effect on cash flow is through the reduction in taxes

- Global’s operating income, EBIT, and pretax income would fall by $1 million because of the $1 million in additional operating expense due to depreciation

- This $1 million decrease in pretax income would reduce Global’s tax bill by 26% ´ $1 million = $0.26 million

- Therefore, net income would fall by 1 - 0.26 = $0.74 million

- On the statement of cash flows, net income would fall by $0.74 million, but we would add back the additional depreciation of $1 million because it is not a cash expense

- Thus, cash from operating activities would rise by -0.74 + 1 = $0.26 million

- Thus, Global’s cash balance at the end of the year would increase by $0.26 million, the amount of the tax savings that resulted from the additional depreciation deduction

- The increase in cash balance comes completely from the reduction in taxes

- Because Global pays $0.26 million less in taxes even though its cash expenses have not increased, it has $0.26 million more in cash at the end of the year