🔎 Operating Cash Flow

From the textbook:

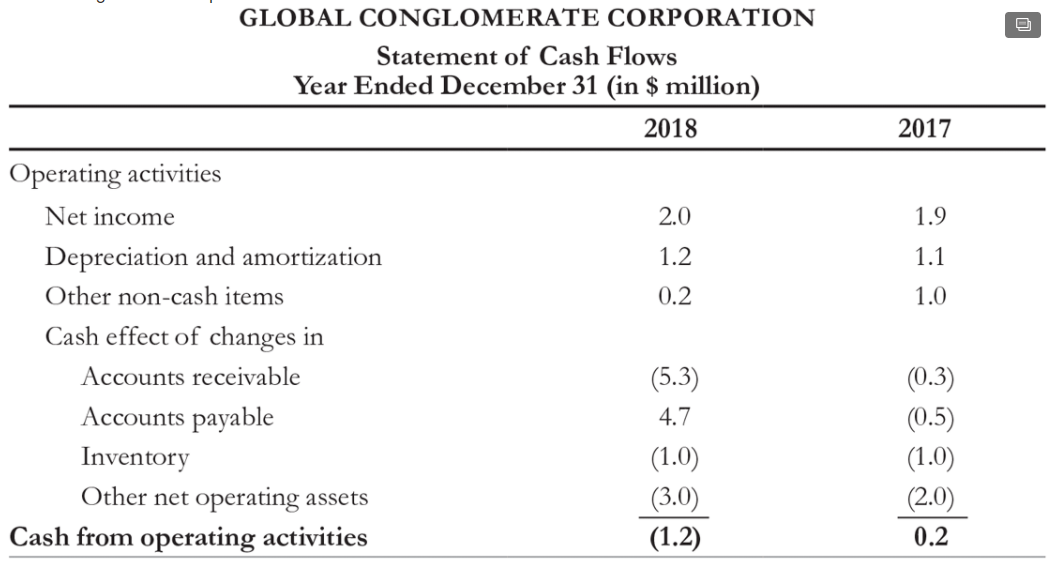

Operating Activity

The first section of Global’s statement of cash flows adjusts net income by all non-cash items related to operating activity. For instance, depreciation is deducted when computing net income, but it is not an actual cash outflow. Thus, we add it back to net income when determining the amount of cash the firm has generated. Similarly, we add back any other non-cash expenses (such as increases in deferred taxes or stock-based compensation expenses).

Next, we adjust for changes to net working capital that arise from changes to accounts receivable, accounts payable, or inventory. Recall that Net Working Capital is defined as follows:

Or, alternatively,

(The second formulation omits notes payable because those are sometimes used as a form of long term financing rather than as a form of working capital.)

Impact of components of ΔNWC on Cash Flow

Accounts Receivable:

- When a firm sells a product, it records the revenue as income even though it may not receive the cash from that sale immediately. Instead, it may grant the customer credit and let the customer pay in the future. The customer’s obligation adds to the firm’s accounts receivable.

- When a sale is recorded as part of net income, but the cash has not yet been received from the customer, we must adjust the cash flows by deducting the increases in accounts receivable. This increase represents additional lending by the firm to its customers, and it reduces the cash available to the firm. In summary when AR ⇧, then Cash Flows ⇩

Accounts Payable:

- Accounts payable are when our company purchases a good but doesn’t pay. Suppose you purchase a truck worth $100,000. Will you have more cash flow now if you pay for the truck with cash or simply promise to pay later. If you promise to pay later, you will have $100,000 more cash flow now. The general idea is that if you can increase AP, you can increase Cash Flow.

- Conversely, we add increases in accounts payable. Accounts payable represents borrowing by the firm from its suppliers. This borrowing increases the cash available to the firm.

Inventory

- Inventory: Next, we deduct increases to inventory. Increases to inventory are not recorded as an expense and do not contribute to net income (the cost of the goods are only included in net income when the goods are actually sold). However, the cost of increasing inventory is a cash expense for the firm and must be deducted.

- Other: Finally, we deduct the increase in any other current assets net of liabilities, excluding cash and debt.

We can identify the changes in these working capital items from the balance sheet. For example, from Table 2.1, Global’s accounts receivable increased from $13.2 million in 2017 to $18.5 million in 2018. We deduct the increase of 18.5−13.2=$5.3 million on the statement of cash flows. Note that although Global showed positive net income on the income statement, it actually had a negative $1.2 million cash flow from operating activity, in large part because of the increase in accounts receivable.

Summary: when you are given ΔNWC

Shortcut: Anything that increases your Net Working Capital will decrease your cash flow.

NWC = Current Assets - Current Liabilities

= Notes Receivable + Accounts Receivable + Inventory - Accounts Payable - Notes Payable.

Anything which causes NWC to ↑ causes Cash flow to ↓.

If AR ↑, that means that CF ↓.

If Inventory ↑, that means that CF ↓.

If AP ↑, that means that CF ↑.

Therefore, we can subtract any change in NWC to see the impact on CF. (But, when in doubt, refer to the material on the left)

The general principle is that anything that decreases the cash the firm has available and can invest or return to stockholders will decrease operating cash flow. In general, anything that increases the NWC that a firm needs will deecrease the free cash that the firm has available. Therefore, it will decrease operating cash flow.

In other words, if the change in Net Working Capital is +$8M (ie ΔNWC=+$8M) then the firm must keep an additional +$8M around to support it’s operations. This cash can’t be used for investments or for returning to stockholders. From the firm’s perspective, it is temporarily gone. It decreases the operating cash flow by $8M.

In formulas:

ΔNWC = $8M Cash Effect of ΔNWC = -$8M

Similarly, if a decreases it’s NWC, then the Cash Effect of this is positive. For example, if purchases a new software product that allows it to collect it’s Accounts Receivable more rapidly, then it will have fewer accounts receivable and more cash. It can take that cash and distribute it to shareholders.

For example, if Accounts Receivable drops by $5M, then NWC will also drop by $5M, because AR is a current asset. In formulas:

Δ AR = -$5M Δ NWC = -$5M Cash Effect of ΔNWC = +$5M

We now have $5M that we can return to shareholders or we can invest profitably within the company. Either way, more Cash, earlier, is good news.

In short, when calculating the Cash Effect of change in Net Working

- Accounts Receivable:

- When a sale is recorded as part of net income, but the cash has not yet been received from the customer, we must adjust the cash flows by deducting the increases in accounts receivable. This increase represents additional lending by the firm to its customers, and it reduces the cash available to the firm. In summary when AR ⇧, then Cash Flows ⇩

- Remember that AR is part of NWC, so when AR ↑, NWC ↑. Based on the “First Way” rule, this means that Cash flows ↓. Therefore, the two rules are compatible.

- Accounts Payable:

- Conversely, we add increases in accounts payable. Accounts payable represents borrowing by the firm from its suppliers. This borrowing increases the cash available to the firm.

- This is consistent with the “first way” rule above. If you increase AP, that will decrease NWC. Decreasing NWC will increase cash flows. Therefore, AP ↑ ⇨ Cash flows ↑. This is why we “add increases in accounts payable.”

Summary:

| NWC↑ | AR↑ | AP↑ | Inventory↑ | |

|---|---|---|---|---|

| Effect on NWC | NWC↑ | NWC↑ | NWC↓ | NWC↑ |

| Effect on Cash Flow | CF↓ | CF↓ | CF↑ | CF↓ |